Zeeshan Khan

Zeeshan Khan Feb 20, 2026

Feb 20, 2026

Table of Contents

Ever feel like your company’s financial records are a puzzle with half the pieces missing? You’re not alone. Many business owners in the UAE start just trying to keep their heads above water, but as the business grows, “keeping the books” turns into a complex maze of regulations.

Without a clear set of rules, how do you even know if your profit is actually profit? That’s where accounting standards come in; they are essentially the universal language of business that ensures everyone is playing by the same rules.

In a global powerhouse like the UAE, these standards aren’t just “nice to have”; they are your ticket to credibility. Whether you are dealing with VAT compliance, seeking a bank loan, or attracting international investors, having standardized reports proves your business is transparent and professional.

Since the UAE is a massive hub for trade and innovation, following these guidelines keeps you competitive and ready for an audit at a moment’s notice. It’s the difference between guessing your way through your finances and having a roadmap to success.

What Are Accounting Standards?

At its simplest, accounting standards are a set of common rules and guidelines that businesses follow when they report their financial results. Think of them as the “grammar and punctuation” of the business world.

Without these rules, one company might record a sale the moment a deal is signed, while another waits until the cash is in the bank, making it impossible to compare the two fairly. These standards ensure that every business is speaking the same financial language.

This consistency is especially important in Accounting for E-commerce Businesses, where transactions happen quickly and across multiple platforms.

Purpose

The main goal of these standards is to keep things honest and clear. They serve three major roles:

- Transparency: They make sure companies aren’t hiding “fine print” or debt in places where investors can’t see it.

- Accuracy: They provide a step-by-step manual for your bookkeeper so that your profit and loss statements reflect the real world, not just a best-case scenario.

- Compliance: They help you meet the legal requirements set by the government, which is especially important for staying on the right side of the law in the UAE.

Regulatory Framework for Accounting in the UAE

Government Role

The UAE regulatory framework takes financial transparency seriously. To maintain its status as a top-tier global business hub, the government provides strict oversight through federal laws. The Ministry of Economy and the Ministry of Finance work together to set the overall direction for Financial Reporting Standards.

Their goal is simple: to make sure every dirham is accounted for and that the UAE economy remains stable, trusted, and attractive to international investors. These regulations also influence the Types of Accounting Services businesses require, from bookkeeping and financial reporting to auditing and tax compliance.

Key Authorities

While the ministries set the big-picture rules, specific authorities handle the day-to-day enforcement. If you are running a business, these are the names you need to know:

- Federal Tax Authority (FTA): They manage everything related to VAT and FTA Corporate Tax.

- Securities and Commodities Authority (SCA): They oversee public joint-stock companies and the markets.

- Central Bank of the UAE: If you’re in the financial or banking sector, they are your primary watchdog.

- Free Zone Authorities: For those in zones like DIFC (regulated by the DFSA) or ADGM (regulated by the FSRA), these bodies have their own specific reporting requirements.

Compliance Importance

Compliance isn’t “one size fits all” in the UAE. Depending on where your license is held, your rules might look a little different:

Especially when you understand the difference between Freezone and Mainland business structures.

| Feature | Mainland Companies | Free Zone Companies |

| Primary Regulator | Department of Economy & Tourism (DET) | Individual Free Zone Authority |

| Audit Requirement | Required if revenue exceeds AED 50 million | Usually mandatory for license renewal |

| Tax Rules | Standard Corporate Tax and VAT | Potential tax holidays (if “Qualifying”) |

| Market Access | Can trade anywhere in the UAE | Primarily international or within the zone |

Staying compliant isn’t just about avoiding fines, it’s about keeping your trade license active. Many free zones won’t let you renew your license without a fresh, audited financial statement. For mainland companies, keeping clean books is your best defense during a routine tax audit

Accounting Standards Followed in the UAE

The UAE doesn’t just use any random system; it follows the global “gold standard.” This ensures that a business in Dubai can be easily understood by an investor in New York or a bank in Singapore.

International Financial Reporting Standards (IFRS)

IFRS is a set of accounting rules used by over 140 countries. It focuses on providing a “true and fair” view of a company’s finances. Instead of just following rigid formulas, it uses principles to ensure the substance of a transaction is recorded, not just the paperwork.

The UAE adopted IFRS to solidify its position as a global financial hub. By using these standards, the country makes it easier for foreign companies to set up shop here and for local companies to attract international investment.

Who must follow the full IFRS?

- Listed Companies: Any business on the Dubai Financial Market (DFM), Abu Dhabi Securities Exchange (ADX), or NASDAQ Dubai.

- Financial Institutions: All banks and insurance companies.

- Large Private Entities: While not always strictly mandated for every small shop, most large mainland and free zone companies use it to satisfy audit and bank requirements.

IFRS for SMEs

Since full IFRS can be incredibly complex and expensive to maintain, the IFRS for SMEs was created. It is a simplified version (about 90% smaller in volume) designed for private companies that don’t have “public accountability” (meaning they aren’t listed on a stock exchange).

Eligibility for SMEs: In the UAE, you are generally eligible to use this simplified version if:

- You do not have shares or debt traded in a public market.

- You are not a bank or insurance company holding money for the public.

For Tax Purposes: The Federal Tax Authority (FTA) allows businesses with a revenue of AED 50 million or less to use IFRS for SMEs for their corporate tax filings.

Key Differences from Full IFRS:

- Simplified Reporting: Many of the complex disclosure requirements are removed.

- Cost Savings: It requires fewer frequent updates and is easier to measure assets.

- Goodwill: Under full IFRS, you test goodwill for “impairment” every year. Under IFRS for SMEs, you simply amortize (spread the cost) over its useful life (usually 10 years).

.

| Feature | Full IFRS | IFRS for SMEs |

| Target Companies | Publicly traded / Large Corps | Private Small/Medium Businesses |

| Complexity | High (3,000+ pages of rules) | Simplified (approx. 250 pages) |

| Reporting Frequency | Updates can happen annually | Updates only every 3–5 years |

| Costs | Higher (requires specialist staff) | Lower (more manageable for small teams) |

Applicability by Business Type

Not every company in the UAE has the same homework when it comes to accounting. Your rules depend largely on where you are registered and how much you earn. Here is how it breaks down for different business types:

Mainland Companies

If your trade license is issued by the Department of Economy and Tourism (DET) in your respective emirate (like Dubai or Abu Dhabi), you are a mainland company.

- Standard: You are generally expected to follow IFRS.

- Audit Rule: Under the UAE Commercial Companies Law, mainland companies must have their accounts audited annually by a licensed auditor.

- Tax Connection: For Corporate Tax filings, you must use these standards to prove your taxable income is accurate.

Free Zone Companies

Businesses in zones like JAFZA, DMCC, or DDA have their own sets of rules governed by their specific Free Zone Authority.

- Audit Requirements: Most free zones require an annual audit to renew your trade license.

- Tax Benefits: To maintain a 0% Corporate Tax rate as a “Qualifying Free Zone Person,” keeping IFRS-compliant books is absolutely mandatory.

- Flexibility: While some zones are strict, others may allow simplified reporting for very small setups, though IFRS remains the default expectation.

Multinational Corporations (MNCs)

For the big players operating across borders, the rules are non-negotiable.

- Full IFRS: MNCs must use full IFRS to ensure their UAE branch or subsidiary “talks” perfectly to the global headquarters.

- Pillar Two Rules: Large groups with global revenues exceeding EUR 750 million (approx. AED 3.15 billion) face even tighter reporting rules under the new global minimum tax standards.

- Consolidation: They must provide detailed reports that allow their parent company to consolidate all profits and losses into one global statement.

SMEs and Startups

The UAE is very supportive of smaller businesses and offers “SME Relief” to keep your costs down.

- IFRS for SMEs: If your revenue is below AED 50 million, you are generally permitted to use the simplified “IFRS for SMEs” framework.

- Cash Basis Accounting: For very small startups with revenue below AED 3 million, the FTA even allows “Cash Basis” accounting, recording money only when it actually hits your bank account, which is much simpler than the standard “Accrual” method.

| Business Type | Common Standard | Mandatory Audit? |

| Mainland LLC | IFRS | Yes |

| Free Zone (QFZP) | IFRS | Yes (to keep 0% tax) |

| Small Startup | Cash Basis / SME IFRS | Usually No (unless license requires) |

| Global MNC | Full IFRS | Yes |

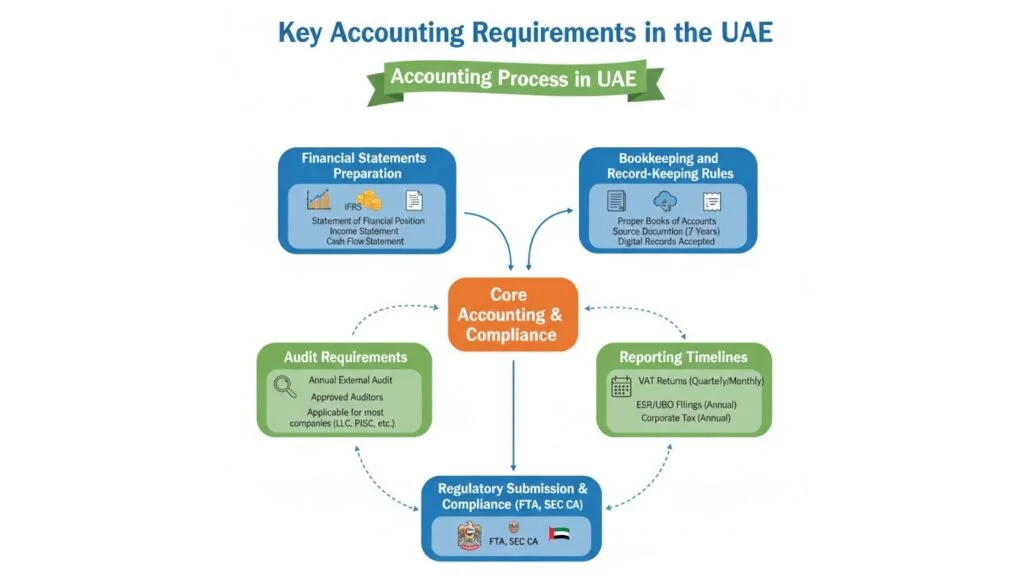

Key Accounting Requirements in the UAE

Running a business in the UAE means keeping your financial house in order. With the introduction of Corporate Tax and stricter global transparency rules, the “wait and see” approach to accounting is a thing of the past. Here is what you need to stay compliant.

Financial Statements Preparation

Every company must prepare a complete set of financial statements at least once a year. These documents tell the story of your business’s health and are required for tax filings and bank reviews. Your package must include:

- Balance Sheet: A snapshot of what you own (assets) and what you owe (liabilities).

- Profit & Loss (P&L): A summary of your revenue and expenses.

- Cash Flow Statement: A report showing how money actually moves in and out.

- Notes to the Accounts: Crucial details that explain the “how” and “why” behind your numbers.

Bookkeeping and Record-Keeping Rules

You can’t just keep receipts in a shoebox. The UAE Federal Tax Authority (FTA) has specific rules about how you track your data:

- Accuracy: Records must demonstrate your financial standing at any given time.

- Retention Period: Under the Commercial Companies Law, you must keep records for 5 years. However, the Corporate Tax Law is stricter, requiring you to hold onto them for 7 years.

- Language: While you can keep daily records in English, the FTA has the right to request an Arabic translation at any time.

Audit Requirements

Is an audit mandatory for everyone? Not necessarily, but it is becoming the standard for many especially when it comes to a small business audit UAE. You must have an audit if:

- Your annual revenue exceeds AED 50 million.

- You are a Qualifying Free Zone Person (to benefit from the 0% tax rate).

- Your specific Free Zone authority requires it for license renewal (common in DMCC, JAFZA, etc.).

- You are a listed company or a branch of a foreign corporation.

Reporting Timelines

Missing a deadline is an expensive mistake in the UAE. Penalties for late filings can be steep and facing a UAE Corporate Tax Penalty can significantly impact your business finances and reputation

- Corporate Tax Return: Must be filed within 9 months from the end of your financial year. For example, if your year ends on December 31, 2025, your deadline is September 30, 2026.

- VAT Returns: Typically due on the 28th day of the month following the end of your tax period (usually quarterly).

- Audit Submissions: Free zone deadlines vary, but many require the audit report within 3 to 6 months after your year ends.

Impact of UAE Corporate Tax on Accounting Standards

With the rollout of the UAE Corporate Tax regime, accounting is no longer just about tracking your profit; it’s a legal necessity. Your financial statements are now the starting point for calculating how much tax you owe the government.

Relationship Between Standards and Corporate Tax

In the UAE, the “Accounting Income” you report in your financial statements is the foundation for your “Taxable Income.” The law (Federal Decree-Law No. 47) specifically requires that your accounts be prepared using IFRS or IFRS for SMEs.

Basically, the Federal Tax Authority (FTA) trusts these international standards to provide a true picture of your business. If your accounting isn’t up to standard, your tax return could be rejected, leading to audits and heavy fines.

Importance of Accurate Records for Compliance

Tax compliance is only as good as your bookkeeping. Accurate records are vital because:

- Evidence in Audits: During a tax audit, the FTA will ask for invoices, bank statements, and ledgers to prove that the numbers on your tax return are real.

- Calculating Adjustments: Not all business expenses are tax-deductible. You need clear records to “add back” items such as 50% of entertainment expenses or fines to your profit before calculating tax.

- Meeting the 7-Year Rule: Under the Corporate Tax law, you must keep all financial records and supporting documents for at least 7 years.

Alignment of IFRS with UAE Tax Laws

While IFRS gives you the “Accounting Profit,” the UAE Tax Law provides specific rules to reach the “Taxable Profit.” Here is how they align:

- Accrual Basis: Both IFRS and the UAE Tax Law prefer the accrual method (recording income when earned, not just when cash hits the bank).

- Fair Value Adjustments: IFRS often requires valuing assets at market price. However, the UAE Tax Law allows you to choose a “realisation basis,” meaning you don’t pay tax on those “on-paper” gains until you actually sell the asset.

- Standardization: Using IFRS ensures that all businesses in the UAE use a consistent language, making it easier for the FTA to verify filings across industries.

| Feature | IFRS Accounting | UAE Corporate Tax |

| Main Goal | Show financial health to stakeholders | Determine the correct tax liability |

| Revenue | Recorded when “earned.” | Recorded when “earned” (Accrual) |

| Fines/Penalties | Deducted as an expense | Not deductible (Must be added back) |

| Entertainment | Fully deductible (usually) | Only 50% deductible |

Common Challenges for Businesses

Running a business in the UAE is exciting, but it’s not without its hurdles. Even the most successful entrepreneurs hit roadblocks when it comes to the “boring” side of business. Here are the most common challenges you might face and how to tackle them.

Lack of Accounting Knowledge

Let’s be honest: you started your business to follow a passion, not to spend hours looking at a ledger. Many business owners struggle with:

- Mixing Finances: Using one bank account for both personal coffee and business inventory makes it impossible to track true profit.

- Incorrect Tax Filings: Misunderstanding what counts as a “taxable supply” can lead to unintentional errors.

- DIY Errors: Using simple spreadsheets instead of FTA-compliant software often leads to data entry mistakes that snowball over time.

Transition to IFRS

If you’ve been using “cash-basis” accounting (recording money only when it hits your account), switching to IFRS can feel like learning a new language.

- The Complexity Gap: Moving to the accrual method requires tracking when service is delivered, not just when it’s paid for.

- Asset Valuation: IFRS requires you to value your assets more precisely, which can be a technical headache if you aren’t an accounting pro.

- System Upgrades: Your old software might not support the detailed reporting IFRS requires, forcing a potentially costly upgrade.

Compliance for New Businesses

When you’re just starting, the sheer number of “to-dos” is overwhelming. Between getting your trade license and finding a space, compliance often slips through the cracks:

- Registration Deadlines: Did you know there are strict windows for Corporate Tax and VAT registration? Missing these can lead to automatic fines of AED 10,000 or more.

- Free Zone vs. Mainland: Understanding which specific rules apply to your location is a common pain point for new arrivals.

Managing Audits and Documentation

An audit shouldn’t be a scary event, but it often is because of poor record-keeping.

- The “Shoebox” Problem: Scrambling to find a receipt from 18 months ago during a tax audit is a nightmare.

- 7-Year Rule: Remembering to keep every single digital and physical record for seven years is a massive organizational challenge.

- Lack of Audit Trails: Auditors need to see who approved a payment and when. If your processes are manual (like via WhatsApp or verbal cues), you won’t have the proof they need.

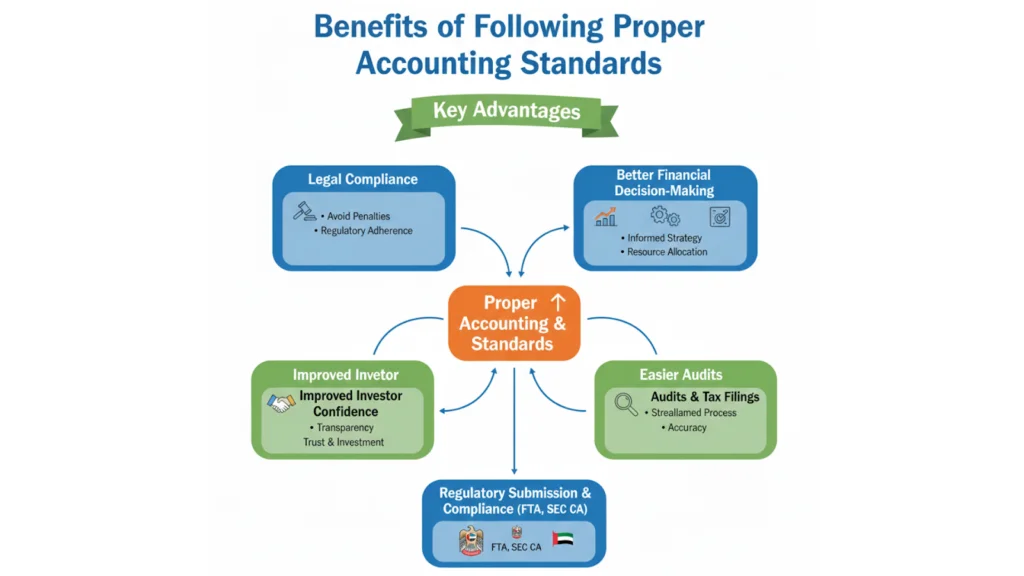

Benefits of Following Proper Accounting Standards

Keeping your finances in order isn’t just about avoiding trouble; it’s about unlocking the full potential of your company. When you move beyond basic spreadsheets and adopt professional standards, you start seeing your business in a whole new light.

| Benefit Area | Key Advantages | Business Impact |

| Legal Compliance | Avoid heavy fines, secure license renewals, and meet all FTA requirements. | Zero Penalties: Stay 100% legal and protected from government checks. |

| Financial Decision-Making | Track profit in real-time, identify wasteful spending, and predict future budgets accurately. | Smarter Growth: Make moves based on real numbers rather than guesses. |

| Investor Confidence | Build professional credibility, gain faster bank loan approvals, and increase company valuation. | Easier Funding: Attract partners and capital with transparent records. |

| Audits & Tax Filings | Reduce auditor fees, ensure quick VAT and Tax submissions, and catch errors early. | Stress-Free Tax: Turn months of “cleanup” work into minutes of filing. |

Role of Professional Accountants and Firms

Why try to do everything yourself when you can have an expert in your corner? As your business grows, the numbers get bigger, and the rules get stricter. Relying on professional help is often the smartest move a business owner can make to ensure nothing falls through the cracks.

Importance of Hiring Professionals

Having a professional accountant is like having a seasoned guide in a complex city. They understand the “why” behind every regulation and can spot potential issues before they turn into expensive fines.

Instead of spending your weekends trying to figure out if your expenses are tax-deductible, a professional handles the technical details so you can focus on your actual work. They bring a level of accuracy that a simple spreadsheet just can’t match, giving you the confidence that your records are audit-ready at all times.

Penalties for Non-Compliance

Staying on the right side of the law is much cheaper than the alternative. In the UAE, the authorities have moved toward a system of high transparency, and they have little patience for businesses that ignore the rules. If you skip out on your accounting duties, the costs can pile up faster than you might think.

Legal and Financial Risks

The biggest risk of non-compliance is the direct hit to your bank account. The Federal Tax Authority (FTA) and other regulators use a structured penalty system to encourage timely reporting.

Beyond just the money, legal risks include the suspension of your trade license. Without a valid license, your entire operation comes to a grinding halt. You can’t process visas, renew office leases, or legally sell your products.

Possible Fines and Consequences

Fines in the UAE are designed to be a serious deterrent. For example, failing to keep proper financial records can result in an initial fine of AED 10,000, which jumps to AED 50,000 for repeat offenses.

Late registration for Corporate Tax carries a heavy price tag, and filing incorrect returns can lead to percentage-based penalties that eat away at your actual profits. In extreme cases of tax evasion, business owners can face court cases and even more severe legal restrictions.

Impact on Business Reputation

Money can be earned back, but a damaged reputation is much harder to fix. When a company is flagged for non-compliance, it sends a red flag to everyone you do business with.

- Banks: They may freeze your accounts or refuse to provide loans if they see you aren’t following the law.

- Suppliers: Major vendors might stop offering you credit terms, demanding “cash on delivery” instead.

- Partners: High-level investors and partners will walk away from a deal the moment they see your books aren’t in order during due diligence.

How Firms Ensure Compliance

Accounting firms stay updated on the latest changes from the Federal Tax Authority and the Ministry of Economy, so you don’t have to. They act as a shield for your business by implementing systems that automatically follow IFRS or UAE Corporate Tax laws.

By conducting regular internal reviews, these firms ensure that every transaction is recorded correctly and that your filings are submitted well before the deadline. This proactive approach turns compliance from a stressful race into a smooth, routine process.

Services Offered

Professional firms provide a full suite of support tailored to your business size. This includes daily bookkeeping to keep your transactions organized and annual audits that provide the official stamp of approval required by free zones and banks.

They also handle complex financial reporting, VAT returns, and Corporate Tax registration. Whether you need a simple monthly check-up or a deep dive into your financial strategy, these services are designed to keep your business healthy and transparent.

Choosing the Right Accounting Consultant in the UAE

Finding the right partner is the final step in securing your company’s financial future. You need a team that doesn’t just crunch numbers but truly understands the local laws and the specific needs of your industry.

By partnering with a firm like HFA Consulting, you gain access to experts who specialize in navigating the complexities of the local market. Choosing professional accounting and bookkeeping services Dubai ensures that your records remain accurate, your taxes are filed on time, and your business stays fully compliant with every new regulation.

Conclusion

Adopting proper accounting standards is the most effective way to protect your business and ensure its long-term success in the UAE’s competitive market. These rules provide the transparency and accuracy needed to satisfy government regulators, secure bank funding, and make informed decisions that drive growth.

Instead of viewing compliance as a burden, see it as a powerful tool that builds professional credibility and keeps your operations running smoothly without the fear of heavy fines.

By staying proactive and keeping your financial records in perfect order, you position your brand as a trusted leader ready for any opportunity the future holds.

FAQs

What are the main accounting standards used in the UAE?

The UAE primarily follows International Financial Reporting Standards (IFRS), with no separate UAE GAAP. Smaller businesses commonly use IFRS for SMEs, a simplified version accepted by the Federal Tax Authority (FTA) and most free zone authorities.

Who must comply with UAE accounting standards?

All registered businesses, including mainland and free zone companies, must maintain proper financial records. Publicly listed companies, banks, and insurance providers are required to use full International Financial Reporting Standards (IFRS) , while private companies and IFRS for SMEs must also comply for legal and tax purposes.

How do accounting standards affect corporate tax in the UAE?

Accounting standards form the basis of corporate tax calculations. The UAE Corporate Tax Law requires taxable income to be calculated using financial statements prepared under IFRS or IFRS for SMEs, ensuring accurate revenue and expense reporting.

What are the consequences of not following accounting standards?

Non-compliance with accounting standards such as International Financial Reporting Standards (IFRS) or Generally Accepted Accounting Principles (GAAP) can result in financial penalties starting from AED 10,000, trade license suspension, and regulatory fines. It may also lead to legal action and mandatory audits.

Zeeshan Khan

My name is Zeeshan Khan, and I’m a UAE-based business and tax consulting professional with hands-on experience in VAT compliance, corporate tax advisory, business setup, and regulatory services. I work closely with startups, SMEs, and established companies to help them navigate UAE tax laws, improve compliance, and make informed financial decisions. With a strong understanding of FTA regulations, corporate structuring, and commercial taxation in the UAE, my focus is on translating complex laws into clear, practical guidance for business owners. Through my writing, I aim to provide accurate, up-to-date insights that help businesses stay compliant, reduce risk, and operate confidently in the UAE market.