Zeeshan Khan

Zeeshan Khan Apr 1, 2026

Apr 1, 2026

Table of Contents

The UAE has long been celebrated as one of the world’s most business-friendly environments. But on 1 June 2023, the country entered a new era of fiscal policy when the federal corporate tax officially came into force. For tens of thousands of businesses operating across the Emirates, understanding and managing corporate tax compliance is no longer optional; it is a legal obligation.

The introduction of corporate tax in the UAE was driven by the country’s commitment to aligning with global tax transparency standards set by the OECD, including the Base Erosion and Profit Shifting (BEPS) framework. It also reflects the UAE’s ambition to diversify government revenue and maintain its competitive edge as a global business hub, while meeting international expectations around fair taxation.

Whether you run a mainland LLC, a free zone entity, or a multinational branch office, your obligations under Federal Decree-Law No. 47 of 2022 are real and enforceable. This guide breaks down everything you need to know, from who pays to how much to what happens if you don’t comply.

Key Takeaways

- UAE corporate tax applies to most businesses and individuals earning above a set threshold from business activity.

- A zero per cent rate applies to income below the lower threshold; only profits above it attract the standard rate.

- Free zone businesses can still benefit from preferential tax treatment, but only if they meet strict Qualifying Free Zone Person conditions.

- Registration with the FTA is mandatory, and missing your deadline triggers immediate financial penalties.

- Tax returns and payments are due within nine months of your financial year-end.

- Small businesses below the revenue threshold may qualify for full relief through the Small Business Relief provision.

- Transfer pricing rules apply to all related party transactions and must be documented properly.

- Records must be kept for a minimum number of years and must be available for FTA audit at any time.

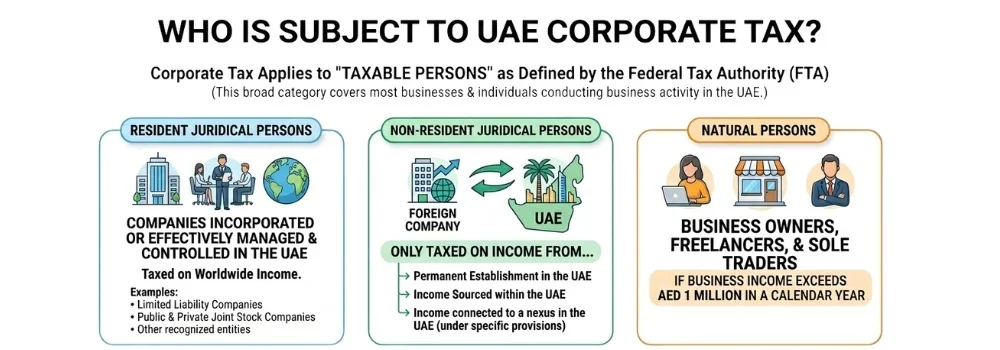

Who Is Subject to UAE Corporate Tax?

Corporate tax applies to what the Federal Tax Authority (FTA) defines as “taxable persons.” This broad category covers most businesses and individuals conducting business activity in the UAE.

Resident juridical persons

Meaning companies incorporated or effectively managed and controlled in the UAE are subject to corporate tax on their worldwide income. This includes limited liability companies, public and private joint stock companies, and other entities recognised under UAE law.

Non-resident juridical persons

Are taxed only on income attributable to a permanent establishment in the UAE, income sourced within the UAE, or income connected to a nexus in the UAE under the law’s specific provisions.

Natural persons

Individual business owners, freelancers, and sole traders are subject to corporate tax if their business income exceeds AED 1 million in a calendar year. This is a notable threshold that brings many self-employed professionals into the tax net for the first time.

Certain categories are explicitly excluded. These include income earned by individuals from employment (salaries, wages, and end-of-service benefits), dividends and capital gains received from qualifying shareholdings, and income from personal investment activity that is not conducted through a licensed business.

Government entities, government-controlled entities meeting specific criteria, extractive businesses subject to Emirate-level taxation, and qualifying public benefit organisations are also generally exempt.

How UAE Corporate Tax Rates and Thresholds Work

The UAE corporate tax rate structure is designed to be straightforward and internationally competitive.

The standard rate is 9% on taxable income exceeding AED 375,000. Taxable income up to that threshold is taxed at 0%, effectively protecting small and micro businesses from any tax burden.

For multinationals that fall within the scope of the OECD’s Pillar Two rules, specifically, multinational enterprise groups with consolidated global revenues of at least EUR 750 million, a different rate of 15% applies under the Qualifying Domestic Minimum Top-up Tax (QDMTT). This ensures that large multinationals pay a minimum effective tax rate even where UAE rates would otherwise fall below that threshold.

These rates place the UAE among the lowest corporate tax jurisdictions globally, preserving its appeal to foreign investors while meeting international commitments.

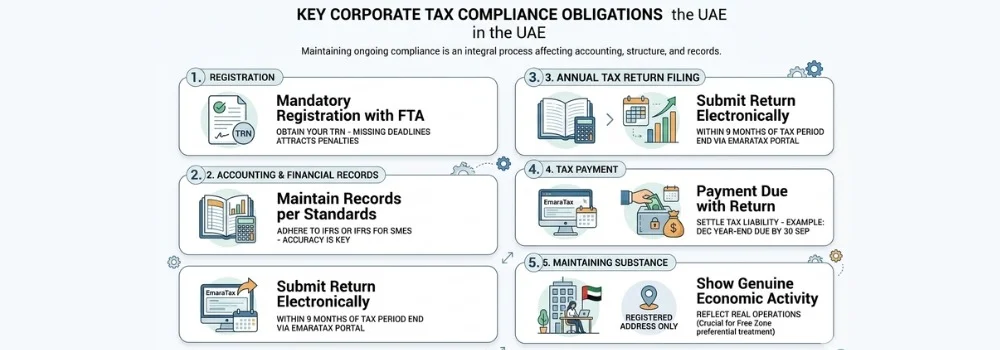

Key Compliance Obligations

Staying compliant with UAE corporate tax law involves more than simply paying a bill once a year. It is an ongoing process that touches your accounting practices, legal structure, and record-keeping systems.

Registration

The first and most time-sensitive obligation. All taxable persons must register with the FTA and obtain a Tax Registration Number (TRN) for corporate tax purposes. Registration deadlines are staggered based on your trade licence issuance date, so missing yours can attract immediate penalties.

Accounting and financial records

Must be maintained in accordance with International Financial Reporting Standards (IFRS) or, for smaller businesses, IFRS for SMEs. Your financial statements form the foundation of your tax return, so accuracy is non-negotiable.

Annual corporate tax return filing

Required for each tax period, which generally corresponds to your financial year. The return must be submitted electronically through the EmaraTax portal within nine months of the end of the relevant tax period.

Tax payment

Due at the same time as the return, nine months after the end of the tax period. This means that if your financial year ends on 31 December, your return and payment are due by 30 September of the following year.

Maintaining adequate substance

Also, a compliance consideration, particularly for free zone businesses claiming preferential treatment. Your UAE operations need to reflect genuine economic activity, not merely a registered address.

How Is Taxable Income Calculated in the UAE?

Taxable income under UAE corporate tax starts with your accounting net profit or loss as reported in your audited financial statements. From there, specific adjustments are made.

Exempt income is excluded. This includes qualifying dividends received from UAE-resident companies and foreign subsidiaries (subject to conditions), qualifying capital gains from the disposal of shares in subsidiaries, and income from international shipping or qualifying aircraft operations under certain criteria.

Non-deductible expenses are added back. These include entertainment expenses (only 50% are deductible), fines and penalties, bribes, and any expenditure not incurred wholly and exclusively for business purposes. Interest deductions are also subject to limitations. The general interest limitation rule caps net interest deductions at 30% of adjusted EBITDA, though businesses with net interest expenditure below AED 12 million are exempt from this cap.

Tax losses from previous periods can be carried forward and offset against a significant portion of taxable income in future tax periods. This provides meaningful relief for businesses that experienced losses in the early years of operation or during difficult trading periods.

Businesses within the same qualifying group can also elect to form a Tax Group, filing a single consolidated return and offsetting profits and losses across group members, which can substantially reduce the overall tax burden.

How UAE Corporate Tax Applies to Free Zone Businesses (QFZP Rules)

One of the most discussed aspects of UAE corporate tax compliance is how it applies to free zone entities. Free zones such as DIFC, ADGM, JAFZA, and over forty others have traditionally offered tax-free environments, and many businesses relocated or established there specifically for that reason.

Under the new law, free zone businesses can still benefit from a 0% corporate tax rate, but only if they qualify as Qualifying Free Zone Persons (QFZPs). The conditions are strict.

To qualify, a free zone entity must maintain adequate substance in the UAE, derive only “qualifying income” (as defined under Ministerial Decision No. 139 of 2023), not elect to be subject to the standard corporate tax regime, comply with transfer pricing rules, and prepare audited financial statements.

Qualifying income broadly covers income from transactions with other free zone persons, income from certain specified activities (such as fund management, reinsurance, logistics, and aircraft engine services), and income from international transactions involving goods that do not enter the UAE mainland market.

If a free zone entity earns income from mainland UAE customers or engages in non-qualifying activities, that portion of income is taxed at the standard 9% rate. This dual treatment requires careful tracking and allocation of income streams.

Failing to meet any one of the QFZP conditions for a tax period can result in the entity losing its qualifying status for that period and the following four tax periods, a significant consequence that underscores the importance of proactive free zone compliance management.

Transfer Pricing and Related Party Transactions

For businesses with related party transactions, whether with parent companies, subsidiaries, affiliated entities, or connected individuals, transfer pricing compliance is a critical component of corporate tax obligations.

The UAE has adopted the OECD Transfer Pricing Guidelines in full. This means that all transactions between related parties must be conducted at arm’s length, that is, on terms that independent parties would agree to under comparable circumstances.

Businesses must maintain a Master File and Local File if their revenue or assets cross certain thresholds, and must be prepared to produce this documentation upon FTA request. Country-by-Country Reporting (CbCR) obligations also apply to qualifying multinational groups.

The FTA has the authority to adjust taxable income where it determines that related party transactions were not priced at arm’s length. This can result in significant upward adjustments to taxable income and corresponding tax liabilities, making proactive transfer pricing documentation not just a compliance formality but a financial risk management measure.

Common related party transactions that attract scrutiny include management fees, intercompany loans, royalties and licensing fees, and the sale or purchase of goods between group entities.

What Are the Penalties for Non-Compliance with UAE Corporate Tax?

The FTA has established a strong penalty framework to enforce corporate tax compliance. These penalties are not symbolic; they are meaningful financial consequences designed to incentivise timely and accurate compliance.

Late registration

carries a fixed administrative penalty per violation. If a business continues to operate without registering, further violations can accumulate quickly, making early registration far cheaper than delay.

Late filing of the tax return

Results in escalating monthly penalties starting at a lower rate in the first year and doubling thereafter. The longer the return remains unfiled, the more costly the position becomes.

Late payment of tax

Triggers percentage-based monthly penalties that begin accruing from the day after the due date. The FTA compounds these charges over time, meaning that an initially manageable liability can grow substantially if left unresolved.

Failure to maintain adequate records

Treated seriously by the FTA, with penalties that double for repeat offences within a two-year window. Businesses that cannot produce records during an audit face both the financial penalty and the risk of estimated assessments on their taxable income.

Voluntary disclosure

The most important tool available to a business that identifies an error or omission after filing. Proactively correcting a mistake with the FTA attracts significantly reduced penalties compared to those imposed when the FTA discovers the same error during an audit. Early self-correction is not just responsible; it is financially strategic.

Tax evasion

sits in an entirely different category. Deliberately concealing income, falsifying records, or providing misleading information to the FTA exposes a business and its directors to the most severe penalties in the framework, potentially including criminal prosecution. No compliance saving is worth that exposure.

Practical Corporate Tax Compliance Checklist

Managing compliance is far easier when broken into concrete, actionable steps. Here is a practical checklist for businesses operating in the UAE:

Before your first tax period

Register with the FTA via EmaraTax before your applicable deadline. Confirm your financial year-end and identify your first tax period. Engage a qualified UAE tax advisor if you do not have in-house expertise.

Assess whether your business qualifies for Small Business Relief or QFZP status. Implement accounting systems capable of producing IFRS-compliant financial statements.

During the tax period

Track all income and expenditure in line with UAE corporate tax rules. Identify and document all related party transactions with proper transfer pricing analysis. Maintain records of any exempt income separately. Monitor interest expenses relative to your EBITDA if you have significant debt financing.

At year-end

Prepare or commission audited financial statements. Prepare your corporate tax return and calculate taxable income. Apply any available tax loss carry-forwards. Submit the return and make payment by the nine-month deadline. Retain all supporting records for a minimum of seven years.

Who Should You Consult for Corporate Tax Compliance in the UAE?

For businesses dealing with UAE corporate tax requirements, HFA Consulting provides structured support to ensure full compliance with local regulations, filing obligations, and reporting standards.

As experienced tax consultants in Dubai, the firm manages corporate tax registration, accurate return filing, transfer pricing documentation, and ongoing compliance requirements in line with Federal Tax Authority guidelines, helping businesses avoid penalties and maintain consistent regulatory compliance.

Conclusion

UAE corporate tax compliance marks a fundamental shift in how businesses in the Emirates must operate. The rates remain internationally competitive, the framework offers meaningful reliefs for small businesses and qualifying free zone entities, and the FTA has provided substantial guidance to help taxpayers navigate the new rules.

But compliance is not passive. It demands proactive registration, robust accounting, careful structuring of related party transactions, and timely filing and payment. Businesses that treat corporate tax as an afterthought rather than an integrated part of financial management face real and escalating financial penalties.

The good news is that for well-organised businesses, UAE corporate tax compliance is entirely manageable. The earlier you build the right systems and seek the right advice, the less disruptive the process will be.

FAQS

When did the UAE corporate tax come into effect?

UAE corporate tax officially came into effect for financial years beginning on or after 1 June 2023. For most businesses with a calendar financial year (1 January to 31 December), the first tax period subject to corporate tax was the year ending 31 December 2024, with returns and payments due by 30 September 2025.

Do freelancers and sole traders have to pay corporate tax?

Yes, in some cases. Natural persons, including freelancers, sole traders, and individual business owners, are subject to corporate tax if their annual business turnover exceeds AED 1 million. Personal income from employment, investment dividends, and real estate held personally (not through a business) is generally excluded.

Are free zone companies exempt from corporate tax?

Not automatically. Free zone companies can access a 0% corporate tax rate, but only if they qualify as Qualifying Free Zone Persons (QFZPs) under the FTA’s conditions. These include maintaining adequate substance, earning only qualifying income, and complying with transfer pricing rules. Income from mainland UAE activities or non-qualifying activities is taxed at 9%.

What is Small Business Relief, and who qualifies?

Small Business Relief allows eligible businesses to be treated as having zero taxable income, effectively paying no corporate tax for a tax period. To qualify, your revenue must not exceed AED 3 million in the relevant tax period and in all prior tax periods from 1 June 2023. This relief is available for tax periods ending on or before 31 December 2026. Businesses that are members of a multinational group with consolidated revenues exceeding EUR 750 million do not qualify.

When do I need to file my corporate tax return?

Your corporate tax return must be filed within nine months of the end of your tax period. For example, if your financial year ends on 31 December, your return is due by 30 September of the following year. Payment is due at the same time as the return.

Is VAT the same as corporate tax in the UAE?

No. VAT (Value Added Tax) and corporate tax are entirely separate taxes administered by the FTA. VAT at 5% applies to the supply of most goods and services and is collected from customers. Corporate tax applies to business profits. A business may be registered for VAT, corporate tax, or both, depending on its activities and revenue.

Can I deduct salaries and rent from taxable income?

Yes. Salaries, wages, rent, utilities, professional fees, and other ordinary business expenses are generally deductible in calculating taxable income, provided they are incurred wholly and exclusively for business purposes and are not specifically disallowed under the corporate tax law. Entertainment expenses are only 50% deductible. Payments to related parties must meet the arm’s length standard to be fully deductible.

What records do I need to keep and for how long?

Businesses are required to retain all records and documents relevant to their corporate tax return for a minimum of seven years from the end of the relevant tax period. This includes financial statements, invoices, contracts, bank statements, payroll records, and transfer pricing documentation. The FTA can request these records during an audit, and failure to produce them attracts penalties.

What happens if I miss the FTA registration deadline?

Missing your corporate tax registration deadline results in an immediate penalty of AED 10,000. If you continue to operate without registering, further violations and penalties can accumulate. It is advisable to register as soon as possible, even if your deadline has passed. Voluntary registration and disclosure generally result in lower penalties than those imposed following an FTA audit or investigation.

Do holding companies or investment vehicles pay corporate tax?

It depends on their structure and activities. Holding companies that receive qualifying dividends and qualifying capital gains from subsidiaries may be able to exempt that income from corporate tax under the participation exemption rules. However, they must still register with the FTA, file returns, and meet the conditions for each exemption claimed. Pure investment holding structures with no employees and no genuine UAE substance should seek specific legal and tax advice to ensure their arrangements remain compliant.

.

Zeeshan Khan

My name is Zeeshan Khan, and I’m a UAE-based business and tax consulting professional with hands-on experience in VAT compliance, corporate tax advisory, business setup, and regulatory services. I work closely with startups, SMEs, and established companies to help them navigate UAE tax laws, improve compliance, and make informed financial decisions. With a strong understanding of FTA regulations, corporate structuring, and commercial taxation in the UAE, my focus is on translating complex laws into clear, practical guidance for business owners. Through my writing, I aim to provide accurate, up-to-date insights that help businesses stay compliant, reduce risk, and operate confidently in the UAE market.