Zeeshan Khan

Zeeshan Khan Mar 16, 2026

Mar 16, 2026

Table of Contents

For a long time, doing business in the Emirates was mostly tax-free, which was a huge draw for entrepreneurs worldwide. However, things changed recently with the introduction of corporate tax in the UAE.

This move was made to bring the country in line with global financial standards and to help the economy grow beyond just oil revenues. It is a big step that shows the UAE is serious about being a transparent and modern place to do business.

This new regime is officially governed by Federal Decree-Law No. 47 of 2022. The law kicked off for financial years starting on or after 1 June 2023, and it is administered by the Federal Tax Authority (FTA).

Generally, if you run a business or perform commercial activities here, whether on the mainland or in a free zone, this likely affects you. With a competitive UAE corporate tax rate of 9% on profits over AED 375,000, the costs are still very low, but you must take corporate tax registration uae seriously.

Ignoring these rules can lead to a heavy UAE corporate tax penalty, so understanding how to stay compliant is the best way to keep your business running smoothly.

Corporate tax in UAE is a direct tax applied to the net profits of businesses operating in the country. Introduced under Federal Decree-Law No. 47 of 2022, it applies to financial years starting on or after 1 June 2023. The standard UAE corporate tax rate is 9% on profits above AED 375,000.

Overview

Under the UAE corporate tax law, businesses are taxed at a 9% federal rate on any profits that go over AED 375,000. This rule started applying to financial years beginning on or after 1 June 2023. If your business makes less than this amount, a 0% rate applies, meaning you won’t pay tax on those initial earnings. Some qualifying free zone companies might also be eligible for this 0% rate, depending on their specific activities.

To figure out what you owe, the tax is calculated based on your net profit after making certain legal adjustments. Even if you fall under the 0% threshold, corporate tax registration UAE is still a mandatory step for most. The entire system is managed by the Federal Tax Authority (FTA), so keeping your records clear and registering on time is the best way to avoid a UAE corporate tax penalty and keep your business in good standing

What Is Corporate Tax in the UAE and How Does It Work?

Simply put, corporate tax is a direct tax on the money a business makes. When a company earns a profit, the government takes a small percentage of that “net income” to help fund public services like roads, schools, and hospitals. It’s the business world’s way of contributing to the country’s growth.

A common question is: “Is this the same as the tax on my salary?” The answer is no. In the UAE, there is no personal income tax. This means your monthly salary, your personal bank interest, and even your personal real estate investments are not taxed. Corporate tax in the UAE is strictly for business activities and is calculated on net profits, which are what is left after you subtract your business expenses from your total sales. Understanding corporation tax advantages every business should know can help companies manage their finances better and stay compliant with UAE regulations.

Examples of what counts as taxable earnings:

- Company Profits: The money your LLC or corporation clears at the end of the year.

- Business Income: Earnings from a commercial activity you run, even as a freelancer (if you pass certain revenue limits).

- Taxable Earnings: Your total revenue minus “allowable deductions” like rent for your office, staff salaries, and marketing costs.

Overview of the UAE Corporate Tax Law

The corporate tax law in the UAE serves as the backbone of the country’s modern fiscal policy. It provides the structured rules and framework that businesses must follow to ensure they are contributing fairly to the national economy.

Federal Decree-Law No. 47 of 2022

This is the primary piece of legislation governing the system. Its purpose is to establish a transparent, competitive, and world-class tax environment. Formalising how business profits are taxed, it helps the UAE align with international standards, boost economic transparency, and diversify government revenue sources beyond traditional sectors.

Role of the Ministry of Finance (MoF)

The Ministry of Finance acts as the “competent authority.” It is responsible for setting the overall tax policy, drafting the necessary legislation, and representing the UAE in international tax treaties. They ensure that the tax regime remains strategic, balanced, and attractive for global investment.

Role of the Federal Tax Authority (FTA)

The Federal Tax Authority (FTA) is the operational arm of the tax system. Think of them as the enforcer and administrator. Their primary duties include:

- Managing tax registration and the issuance of Tax Registration Numbers (TRNs).

- Overseeing the filing and processing of tax returns.

- Enforcing compliance through audits and ensuring that penalties for non-compliance are applied correctly.

- Providing public guidance to help businesses understand their obligations.

When the Law Came Into Effect

The law was enacted to apply to all businesses for their first financial year starting on or after 1 June 2023.

- 31 January 2022: Official announcement of the upcoming Federal Corporate Tax.

- 9 December 2022: Official issuance of Federal Decree-Law No. 47 of 2022.

- 1 June 2023: The law officially becomes effective for the first applicable financial periods.

UAE Corporate Tax Rate Explained

The UAE corporate tax system is designed to be straightforward and competitive, ensuring that businesses can continue to grow while contributing to the nation’s economy. The structure is tiered to protect smaller entities while maintaining a fair tax baseline for larger organisations.

| Taxable Income | Corporate Tax in UAE Rate |

| Up to AED 375,000 | 0% |

| Above AED 375,000 | 9% |

Why This Threshold Exists

The AED 375,000 threshold acts as a buffer for the business community. By applying a 0% tax rate to this initial amount, the government ensures that the vast majority of small businesses and startups are not burdened by immediate tax payments during their critical early growth stages.

This “tax-free” portion essentially covers basic operational costs and profit margins for smaller ventures, allowing them to reinvest their earnings back into the business.

Support for Startups and SMEs

Beyond the standard threshold, the UAE has introduced specific programs like the Small Business Relief, which is available to qualifying entities with annual revenues below AED 3 million until the end of 2026.

These measures highlight the government’s commitment to maintaining a business-friendly environment where innovation and entrepreneurship are encouraged rather than penalised.

The OECD Global Minimum Tax

While the UAE’s standard rate is 9%, it is important to note the global context. Under the OECD’s Pillar Two framework, very large multinational enterprise (MNE) groups those with consolidated global revenues exceeding EUR 750 million may be subject to a 15% global minimum tax.

To ensure that this tax revenue stays within the UAE rather than being collected by foreign tax authorities, the UAE has implemented a Domestic Minimum Top-up Tax (DMTT) for these large groups. For the vast majority of local businesses and SMEs, however, the standard 0% and 9% rules remain the primary focus.

Who Needs to Pay Corporate Tax in the UAE?

In the UAE, corporate tax applies broadly to almost all businesses and commercial activities. Whether you operate as a large corporation, a small family business, or an individual freelancer, it is important to determine your status under the law.

Mainland Companies

If your business is registered with an economic department in any of the seven emirates, it is considered a mainland company. All such businesses are subject to the UAE corporate tax regime. This means you must register for a Tax Registration Number (TRN), keep accurate financial records, and file an annual tax return with the Federal Tax Authority (FTA).

Free Zone Companies

Free Zone Companies registered in the UAE are also within the scope of the corporate tax law. However, they may benefit from a 0% tax rate if they qualify as a Qualifying Free Zone Person (QFZP). To maintain this 0% status, you must maintain adequate substance in the free zone, such as proper office space and qualified staff.

You must also generate Qualifying Income, which is mainly from activities outside the UAE or with other free zone entities. Additionally, you must adhere to strict transfer pricing rules and maintain audited financial statements. If these conditions are not met, the free zone company will be subject to the standard 9% corporate tax rate. These rules are part of the UAE free zone tax regulations that businesses must follow to continue benefiting from the available tax incentives.

Foreign Companies Operating in the UAE

A foreign company that does not have a physical headquarters in the UAE may still be liable for corporate tax if it has a Permanent Establishment (PE) in the country.

This generally occurs if the foreign entity has a fixed place of business in the UAE, such as an office, branch, or workshop. It also applies if the company operates through a dependent agent in the UAE who has the authority to habitually conclude contracts on behalf of the company. If a PE exists, the income attributed to that UAE-based activity is subject to corporate tax.

Freelancers and Sole Establishments

Many individuals are surprised to learn that they can be subject to corporate tax in the UAE. If you operate as a “natural person” conducting a business activity, such as a freelancer, consultant, or sole proprietor, you are within the scope of the law.

You are generally required to register for corporate tax if your total annual revenue from business activities exceeds AED 1 million. Once you are registered, the standard rules apply to your taxable income.

The first AED 375,000 of your net profit is taxed at 0%, and any net profit above that is taxed at 9%. If your total annual revenue is below AED 1 million, you currently do not need to register for corporate tax, even if you are operating a business activity.

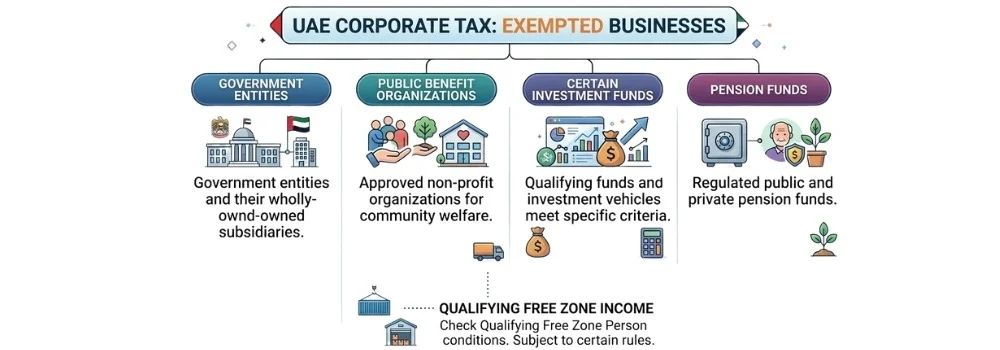

Businesses Exempt from Corporate Tax

While the corporate tax law in the UAE is comprehensive, it does not apply to everyone. Certain entities are classified as “Exempt Persons” because they serve specific public, social, or governmental interests.

These entities are not subject to the standard corporate tax requirements, though some may still need to fulfill specific registration or notification obligations depending on their status.

Government Entities

Federal and local government entities, as well as government-controlled entities, are generally exempt from corporate tax. This is because these organizations exist to serve the public interest and carry out sovereign or government-mandated activities.

If these entities perform certain commercial activities, however, those specific activities might be treated as an independent business and could potentially be subject to tax.

Public Benefit Organizations

Organizations that are established exclusively for public welfare, such as registered charities and non-profit organizations, can qualify for an exemption.

To benefit from this, they must be listed in a formal Cabinet Decision and prove that their income is used strictly for their charitable or social goals. They cannot distribute profits to any private members, shareholders, or founders.

Certain Investment Funds

Qualifying Investment Funds can apply for an exemption from corporate tax. To qualify, these funds typically need to be regulated by a competent authority in the UAE or a recognized foreign regulatory body.

They must be set up to pool investor capital and should not be created for the primary purpose of tax avoidance.

Pension Funds

Public and private pension or social security funds are also exempt. This exemption recognizes the critical role these funds play in providing financial security for retirees and employees.

These funds must meet specific regulatory requirements to ensure they are genuinely serving their purpose of managing retirement savings or end-of-service gratuities.

Qualifying Free Zone Income

It is important to clarify that free zone companies are not automatically “exempt” in the same way as government bodies. However, a Qualifying Free Zone Person (QFZP) can benefit from a 0% tax rate on their qualifying income, which is considered one of the key benefits of free zone company in Dubai. This is a specific tax incentive rather than a blanket exemption.

To maintain this 0% status, these companies must meet strict conditions regarding their business presence, the nature of their income, and compliance with transfer pricing regulations. If these requirements are not met, their income becomes subject to the standard 9% corporate tax rate.

Corporate Tax Registration in the UAE

Staying compliant with tax laws is essential for any business operating in the Emirates. Proper registration is not just a legal requirement; it is your gateway to maintaining good standing with the authorities and avoiding unnecessary financial strain.

What Is Corporate Tax Registration

Corporate tax registration is the official process of registering your business with the Federal Tax Authority (FTA). Once you complete this process, you are issued a unique Corporate Tax Registration Number (TRN).

This number is vital, as you will need it for all your future tax filings, correspondence with the FTA, and any other regulatory obligations related to your business’s tax status. Even if your business qualifies for a 0% tax rate, you are generally still required to register.

Where to Register

All corporate tax registration in the UAE is handled online through the official FTA portal, known as EmaraTax. This user-friendly platform serves as the central hub for all your tax-related needs, from registration to filing returns. To get started, you can log in using your existing FTA account credentials or your UAE Pass for a faster, more secure experience.

Documents Required

To ensure your application is processed without delays, you should have your documentation ready before you begin. The FTA requires clear and valid copies of your official papers, which typically include:

- Trade License: A current, valid copy of your commercial license.

- Emirates ID: Copies for all business owners or shareholders who are UAE residents.

- Passport Copy: Valid passport copies for all business owners or shareholders.

- Financial Details: Documents such as your profit and loss statements or other financial records that verify your business income and structure.

- Proof of Authorization: Documents like a Power of Attorney, board resolution, or the relevant sections of your Memorandum of Association (MOA) that show who is authorized to sign on behalf of the company.

If you need professional support with the registration process, working with an experienced tax consultant in Dubai can help ensure your corporate tax registration is completed correctly and on time.

Corporate Tax Registration Deadlines

The Federal Tax Authority has set specific timelines for registration, and meeting these is critical. If your business was established on or after March 1, 2024, you are generally required to register within three months of your incorporation or establishment date. For older entities, deadlines were staggered based on the month your commercial license was issued.

It is important to stay proactive because failing to register by the deadline can lead to an administrative penalty of AED 10,000. Because these deadlines can vary based on your specific legal structure and license date, it is a good practice to check your exact status on the EmaraTax portal or consult with a tax professional to ensure you remain fully compliant and penalty-free.

Businesses in the UAE must comply with specific deadlines under the corporate tax regime. The most important timelines include corporate tax registration deadlines set by the Federal Tax Authority and the annual filing deadline for corporate tax returns.

Corporate tax returns must generally be filed within nine months after the end of the financial year. Missing these deadlines can result in administrative penalties.

How to Calculate Corporate Tax in UAE

Calculating your corporate tax liability might seem complex at first, but it follows a structured, step-by-step approach.

Because your accounting profit is not always the same as your taxable income, the process involves a few specific adjustments to ensure you are reporting the correct figures to the Federal Tax Authority (FTA).

Determine Accounting Profit

The starting point for your calculation is your company’s net profit or loss as reported in your annual financial statements.

These statements must be prepared in accordance with internationally accepted accounting standards, such as the International Financial Reporting Standards (IFRS) or the IFRS for SMEs. This figure serves as the baseline for your tax assessment.

Adjust for Taxable Income

Since accounting profit includes everything from non-taxable income to non-deductible expenses, you must make “tax adjustments” to bridge the gap between your bookkeeping and the tax law.

Common adjustments include adding back expenses that the FTA does not allow, such as administrative fines, specific entertainment costs, or personal expenditures.

Conversely, you will subtract income that is legally exempt from corporate tax, such as qualifying dividends or certain foreign income. Once you apply these additions and subtractions, the resulting figure is your “Taxable Income.”

Apply Corporate Tax Rate

Once you have determined your final Taxable Income, you apply the tiered tax rates. The first AED 375,000 of your taxable income is taxed at 0%, meaning you pay no corporate tax on this portion. Any amount exceeding this threshold is then subject to the 9% corporate tax rate.

| Net Profit | Taxable Portion | Corporate Tax |

| AED 300,000 | 0 | 0 |

| AED 500,000 | 125,000 | AED 11,250 |

In the example of an AED 500,000 profit, the first AED 375,000 is tax-free. The remaining AED 125,000 is then multiplied by 9%, resulting in a total tax liability of AED 11,250.

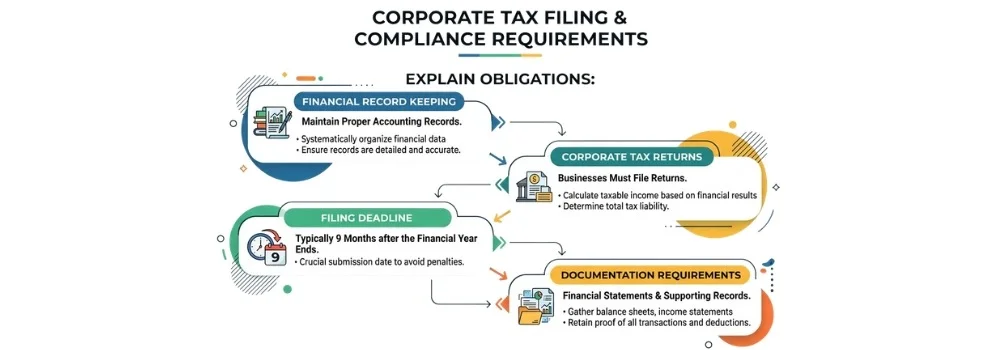

Corporate Tax Filing and Compliance Requirements

Staying compliant with the UAE’s corporate tax regime requires more than just paying your dues; it demands consistent financial discipline. The Federal Tax Authority (FTA) requires all taxable persons to maintain transparency, ensuring that every transaction is documented and that financial reports accurately reflect their business activities.

Financial Record Keeping

You must maintain proper accounting records that accurately represent your business’s financial position. These records serve as the foundation for your tax calculations.

It is a legal requirement to retain all financial statements, invoices, receipts, contracts, and other supporting documents for a minimum of seven years from the end of the relevant tax period.

This rigorous record-keeping is not just for the FTA; it acts as a safeguard, ensuring you are always prepared for an audit and can easily substantiate your reported income and deductions.

Corporate Tax Returns

Every business entity subject to corporate tax must file an annual Corporate Tax Return with the FTA. This return is the formal declaration of your business’s financial performance, taxable income, and the tax liability calculated for that period.

Even if your business is eligible for a 0% tax rate, you are still required to file this return to confirm your status and transparency.

Filing Deadline

The general rule is that your Corporate Tax Return must be filed and any tax due must be paid within nine months after the end of your financial year. For example, if your financial year aligns with the calendar year and ends on 31 December, your deadline for filing and payment is 30 September of the following year.

It is vital to track this deadline based on your specific financial year to avoid administrative penalties and late payment interest.

Documentation Requirements

When filing, you will need more than just a final profit figure. You should be ready to provide a comprehensive set of documents that justify your tax position. This includes audited or management-prepared financial statements, a breakdown of taxable vs. exempt income, and detailed schedules for any adjustments made to your accounting profit.

If you are part of a group or engaged in transactions with related parties, you may also need to provide Transfer Pricing documentation. Keeping these documents organized throughout the year will make the filing process significantly faster and less stressful when the deadline approaches.

Many businesses rely on expert tax consultancy services in Dubai to manage ongoing corporate tax compliance and avoid administrative penalties.

UAE Corporate Tax Penalties

Operating in the UAE requires a clear understanding of your fiscal responsibilities. The Federal Tax Authority (FTA) enforces strict compliance to ensure transparency and fairness across the business landscape.

If a business fails to adhere to the law, it faces a range of administrative fines, known as a UAE corporate tax penalty. Staying aware of these risks is the best way to safeguard your company’s financial health.

Late Registration Penalty

Registering your business is a fundamental step, and missing the corporate tax registration UAE deadline set by the FTA can come with a high cost. Failing to submit a corporate tax registration application on time generally results in an administrative penalty of AED 10,000.

While the government has introduced temporary waiver initiatives in specific circumstances for first-time filers, relying on these is risky. Proactive registration is the only reliable way to avoid this fine and ensure your business remains in good standing.

Late Tax Filing

Timely submission of your Corporate Tax Return is non-negotiable. If you fail to file your return by the designated deadline, the FTA imposes a penalty of AED 500 per month for the first 12 months of delay.

If the delay extends beyond one year, this fine increases to AED 1,000 per month. These penalties start the day after your filing deadline and accumulate monthly, quickly turning into a significant financial burden.

Incorrect Reporting

Accuracy is just as important as timeliness. If you submit a tax return that contains errors or misreported income, you may be subject to a fixed penalty of AED 500. While this may seem small, it serves as a warning.

If the incorrect filing leads to a significant discrepancy in tax liability and is discovered by the FTA after the submission deadline, you could face much steeper percentage-based penalties on the tax difference. It is always better to correct any identified errors through a voluntary disclosure before the FTA initiates an audit.

Failure to Maintain Records

The law requires every business to keep accurate, organized financial records for at least seven years. These records are the evidence that justifies your tax filings. If the FTA finds that your records are inadequate, incomplete, or missing, they may impose a penalty of AED 10,000 for the first violation.

If this happens again within 24 months, the fine doubles to AED 20,000. Keeping your bookkeeping clean is an essential operational habit that protects you from these avoidable costs.

UAE Corporate Tax Compliance Checklist

Staying compliant with the UAE’s corporate tax regime requires consistent financial discipline and a clear understanding of your obligations. Use this checklist to ensure your business remains in good standing with the Federal Tax Authority (FTA).

| Compliance Area | Key Action Items |

| Registration | Register on the EmaraTax portal and obtain your Tax Registration Number (TRN). |

| Record Keeping | Maintain accurate financial records (invoices, ledgers, contracts) for at least 7 years. |

| Income Assessment | Calculate net profit per IFRS standards and adjust for non-deductible expenses. |

| Reporting | Prepare annual financial statements; ensure audits are done if revenue thresholds are met. |

| Filing | File your Corporate Tax Return electronically within 9 months of your financial year-end. |

| Payment | Settle any tax liabilities concurrently with your tax return submission. |

| Transfer Pricing | Document all related-party transactions to align with the “arm’s length” principle. |

| Exemption/Relief | Verify and document eligibility for Small Business Relief or Qualifying Free Zone status. |

Corporate Tax Planning Strategies for UAE Businesses

Strategic tax planning allows businesses to manage their finances in a way that remains fully compliant with the UAE corporate tax law while legally minimizing the tax burden. Proactive management ensures your company retains more profit for reinvestment and growth.

Small Business Relief

The Small Business Relief (SBR) initiative is a key incentive for resident businesses and individuals with annual revenue not exceeding AED 3 million. By electing for this relief when filing your tax return, your business is treated as having no taxable income for that period.

This removes the need for complex tax calculations and reduces your administrative burden. This relief is available for tax periods ending on or before 31 December 2026, and you must proactively opt into it through the EmaraTax portal.

Allowable Expense Deductions

Lowering your tax bill often comes down to accurately identifying every legitimate business expense. An expense is generally “allowable” if it is incurred wholly and exclusively for your business operations.

Common deductible items include staff salaries and benefits, commercial rent, utilities, marketing costs, and depreciation on fixed assets. Keeping meticulous records of these expenditures ensures you can substantiate your deductions and reduce your overall taxable profit.

Loss Carry-Forward Rules

If your business experiences a tax loss, you are not simply stuck with that burden. The UAE regime allows you to carry forward these losses to offset taxable income in future profitable years.

You can utilize these losses to reduce your taxable income by up to 75% in any given subsequent tax period. The remaining unutilized losses can be carried forward indefinitely, provided you maintain accurate records and satisfy ownership continuity requirements.

Group Relief

For companies operating with multiple entities, forming a Tax Group is a powerful tool for optimization. A Tax Group allows the parent company and its subsidiaries to be treated as a single taxable person, simplifying your administrative filing. This structure enables the internal transfer of tax losses between members, which can effectively lower the total tax payable by the group.

To qualify, the parent company generally must own at least 95% of the subsidiary’s share capital, voting rights, and profits, and all members must follow the same financial year and accounting standards.

Common Corporate Tax Mistakes Businesses Make

Even the most organized businesses can stumble when navigating the complexities of the UAE’s corporate tax regime. Identifying these common pitfalls early can save you significant time, money, and stress.

Late Registration

Many businesses mistakenly believe that they can wait until they are ready to file their first tax return to register. However, registration is a distinct legal obligation. Failing to register for corporate tax within the timeframes specified by the Federal Tax Authority (FTA) can result in a fixed administrative penalty of AED 10,000.

It is essential to monitor your license issuance date and register well before your deadlines to avoid this immediate financial blow.

Poor Bookkeeping

Corporate tax calculations rely entirely on the quality of your financial data. Businesses often fail because they rely on outdated spreadsheets, mix personal and business expenses, or lack the supporting documentation (such as contracts and receipts) required to substantiate their figures.

Under the law, you must maintain your financial records for at least seven years. Without organized, audit-ready books, you risk incorrect filings, which can invite deeper scrutiny from the FTA during an audit.

Misunderstanding Free Zone Rules

A prevalent misconception is that operating within a Free Zone automatically grants a total tax exemption. In reality, while Qualifying Free Zone Persons may benefit from a 0% tax rate, this status is conditional.

Failing to meet the “adequate substance” requirements, misclassifying non-qualifying income, or failing to file an annual tax return can retroactively disqualify you from this benefit. Once disqualified, you could be subject to the full 9% tax rate on all your income, which creates a substantial and unexpected tax liability.

Incorrect Profit Calculation

Many business owners incorrectly assume that the profit shown on their internal management reports is their taxable income. Accounting profit often includes items that are non-deductible or exempt, requiring specific adjustments to arrive at the correct taxable income.

For instance, claiming non-deductible expenses like traffic fines or personal expenditures as business costs is a frequent error. When the FTA identifies these discrepancies, it leads to reassessments, interest charges, and potential penalties for underpayment.

Consequences of Non-Compliance

The consequences of these mistakes extend beyond simple fines. Persistent errors can strain your cash flow due to cumulative interest (calculated at 14% per annum on unpaid tax), damage your reputation with investors and banks, and significantly increase your risk of being selected for a comprehensive tax audit.

In severe cases, repeated non-compliance can even lead to the suspension of your trade license. Proactive tax management and regular consultations with a tax professional are the best ways to mitigate these risks and ensure your business stays focused on growth rather than remediation.

How a Tax Consultant Helps Businesses Stay Compliant

The UAE corporate tax regime can be challenging, especially as regulations evolve to meet international standards. Many companies work with a professional tax consultant in Dubai to ensure compliance with UAE corporate tax regulations and avoid costly penalties.

By partnering with experts, business owners can shift their focus back to core operations while maintaining full confidence in their financial standing.

Corporate Tax Advisory

Tax consultants provide deep technical insight into the nuances of the law. They help you interpret how specific regulations apply to your unique business model, whether you are a small startup or a large enterprise.

This advisory covers everything from understanding your tax base to clarifying complex provisions regarding related-party transactions and international tax treaties.

Compliance Support

Staying compliant is more than just filing a return; it requires meticulous, ongoing management. A consultant ensures that your company adheres to all legal requirements, including maintaining adequate “economic substance” and following strict record-keeping protocols.

They act as your representative, ensuring that all submissions to the Federal Tax Authority (FTA) are prepared accurately and filed well before any deadlines.

Tax Planning

Beyond ensuring you follow the rules, tax planning is about long-term financial health. Consultants analyze your financial structure to identify legitimate tax-saving opportunities.

This includes advising on the best use of Small Business Relief, loss carry-forward strategies, or the benefits of forming a Tax Group. Their goal is to help you optimize your cash flow while ensuring all tax-efficiency strategies remain fully aligned with legal standards.

FTA Registration Assistance

The registration process on the EmaraTax portal can be confusing, particularly when determining the exact classification of your business or verifying your eligibility for specific reliefs.

A consultant handles the entire registration workflow, ensuring that the information provided is consistent with your trade license and business structure. This eliminates the risk of errors and minimizes the potential for delays in obtaining your Tax Registration Number (TRN).

Who Should Businesses Consult for Corporate Tax Matters?

Businesses in the UAE should engage experienced professionals to ensure accurate financial reporting and full regulatory adherence in a tax landscape that demands precision.

Partnering with qualified corporate tax consultants in Dubai, such as HFA Consulting, provides essential expertise in identifying taxable income, navigating complex exemption rules, and implementing effective tax planning strategies.

By benefiting from the specialized knowledge of FTA-registered agents, companies can streamline their registration and filing processes, mitigate the risk of costly penalties, and optimize their tax positions to support sustainable, long-term growth.

Conclusion

Successfully managing corporate tax in the UAE is essential for maintaining your business’s credibility, avoiding severe administrative penalties, and ensuring long-term financial health.

As the tax landscape continues to mature, compliance requirements ranging from accurate bookkeeping and timely registration to precise profit reporting have become critical pillars of operational integrity.

Given the complexities involved in navigating exemptions, reliefs, and evolving regulatory standards, seeking professional guidance from established experts like HFA Consulting is a strategic move that helps you mitigate risks and optimize your tax position.

We encourage all business owners to stay proactively informed about legislative updates and prioritize robust financial practices to ensure your enterprise remains compliant, efficient, and well-positioned for sustainable growth in the UAE.

FAQS

When did corporate tax start in the UAE?

The UAE’s federal corporate tax regime was formally introduced under Federal Decree-Law No. 47 of 2022 and became effective for financial years starting on or after June 1, 2023, with the specific implementation date for each entity depending on its established financial accounting period.

What is corporate tax in the UAE?

Corporate tax is a direct tax levied on the net income or profits of businesses and other entities, designed to align the UAE with international best practices and diversify government revenue.

What is the corporate tax rate in the UAE?

The standard corporate tax rate is 9% on taxable income exceeding AED 375,000, while a 0% rate applies to taxable income up to that threshold.

Do free zone companies pay corporate tax?

Yes, they are subject to corporate tax, though “Qualifying Free Zone Persons” may benefit from a 0% preferential tax rate on their “Qualifying Income” if they meet specific substance and activity requirements.

What is the corporate tax threshold in the UAE?

The 0% tax rate applies to the first AED 375,000 of taxable income, and the 9% rate applies to any taxable income above that amount.

Is corporate tax mandatory for all businesses?

Registration is mandatory for almost all businesses and commercial activities, including mainland companies, free zone entities, and certain individuals engaged in business, regardless of their revenue or tax liability status.

What happens if a company fails to register for corporate tax?

Failure to register on time results in a fixed administrative penalty of AED 10,000, and further non-compliance can lead to additional fines, interest on unpaid taxes, and potential operational restrictions.

Can businesses reduce corporate tax legally?

Yes, businesses can legally manage their tax liability by ensuring all eligible business expenses are deducted, utilizing Small Business Relief if eligible, carrying forward tax losses to future years, or forming a Tax Group for consolidated reporting.

How to register for corporate tax in UAE?

Businesses must register electronically through the official FTA EmaraTax portal using their FTA credentials or UAE Pass, where they will submit required business and identification documents to obtain a Tax Registration Number (TRN).

Do private banks have to pay corporate taxes in the UAE?

Yes, commercial banks and financial institutions, whether operating in the mainland or free zones, are generally considered taxable persons and must comply with standard corporate tax registration and filing requirements.

Zeeshan Khan

My name is Zeeshan Khan, and I’m a UAE-based business and tax consulting professional with hands-on experience in VAT compliance, corporate tax advisory, business setup, and regulatory services. I work closely with startups, SMEs, and established companies to help them navigate UAE tax laws, improve compliance, and make informed financial decisions. With a strong understanding of FTA regulations, corporate structuring, and commercial taxation in the UAE, my focus is on translating complex laws into clear, practical guidance for business owners. Through my writing, I aim to provide accurate, up-to-date insights that help businesses stay compliant, reduce risk, and operate confidently in the UAE market.