Zeeshan Khan

Zeeshan Khan Feb 25, 2026

Feb 25, 2026

Table of Contents

Are you living or running a business in Sharjah, UAE, but still worried about getting taxed back home? It’s a common headache. You’ve done the hard work of setting up in a tax-friendly environment, yet foreign tax authorities might still come knocking.

That is exactly where a Tax Residency Certificate (TRC) comes in. Think of it as your official “get out of jail free” card that proves you are a legal tax resident of the UAE, protecting your hard-earned money from being taxed twice.

But how do you actually get one without drowning in paperwork? Whether you’re a freelancer, an employee, or a business owner, having this piece of paper is a defining moment.

It opens the power of the UAE’s massive network of double taxation treaties, making sure you keep what you earn. From gaining instant credibility with international banks to saving thousands in potential tax leaks, the TRC is the ultimate tool for financial peace of mind.

What is a Tax Residency Certificate?

If you’ve ever felt like the rules of international money are written in a different language, you aren’t alone. One term you’ll hear constantly in the Emirates is the Tax Residency Certificate (TRC). But what is it, really?

In simple terms, it is an official document issued by the UAE authorities (specifically the Federal Tax Authority) confirming that a person or a company is a legal tax resident in the UAE. Think of it as your official “ID card” for taxes. It’s the paper that tells the rest of the world that you belong to the UAE tax group system.

Purpose: Why Do You Need It?

You might be wondering, “If I live here, isn’t that enough?” Unfortunately, most foreign tax offices need more than just a copy of your visa or a photo of you at the beach. They need government-backed proof to stop sending you tax bills.

The TRC serves two main purposes:

- Proving Residency: It acts as the ultimate evidence for foreign tax departments, showing that you are a resident here for tax purposes and not just a visitor.

- Accessing DTAA Benefits: The UAE has signed Double Taxation Avoidance Agreements (DTAA) with over 130 countries. These are essentially “handshake deals” between nations to ensure you don’t get taxed twice on the same income. The TRC is the tool that triggers these benefits, allowing you to claim exemptions or lower tax rates abroad.

Essentially, the TRC is your shield. It keeps your money where it belongs with you, rather than letting it leak away to a country you no longer live in.

Who Can Apply for a TRC in the UAE?

Wondering if you qualify? The UAE has made it easier than ever to prove your tax status, but there are a few boxes you need to tick first. Generally, if you call the UAE home or run a business here, you are likely eligible.

For Individuals: Is the UAE Your Main Hub?

If you are an expat, a GCC national, or a UAE citizen, you can apply for this certificate. However, it isn’t just about having a visa; it’s about how much time you actually spend in the country. To qualify, you typically need to meet one of these residency tests:

- The 183-Day Rule: You have been physically present in the UAE for at least 183 days over 12 months.

- The 90-Day Rule: You have been in the UAE for 90 days or more, hold a valid residency visa, and either have a permanent place to live (like a rental or owned home) or a job/business here.

- Primary Residence: You can show that the UAE is your primary place of residence and the center of your financial and personal interests.

For Companies: Are You Established Here?

Businesses can also apply to protect their corporate income. Whether you are a Mainland company or based in a Free Zone, you are eligible as long as you meet these criteria:

- Operational History: Your company must have been active and established in the UAE for at least one year.

- Management & Control: You must show that the business is actually managed and controlled from within the UAE (not just a “paper company”).

- Physical Office: You need a physical office space and a valid trade license.

Note: Offshore companies are generally not eligible for a TRC because they lack a physical presence in the country.

Understanding the Difference Between Freezone and Mainland

It’s important to know the difference between Freezone and Mainland companies, as it can affect your eligibility, tax obligations, and operational flexibility. Mainland companies can trade anywhere in the UAE, while Freezone companies have certain restrictions but may benefit from tax incentives and full foreign ownership.

Eligibility Criteria

Are you wondering if you qualify? While the UAE is famous for its tax-friendly environment, the Federal Tax Authority (FTA) has specific rules to ensure only true residents get a certificate. It’s not just about having a visa; it’s about proving your “economic heart” is in the Emirates.

For Individuals: The 183-Day Gold Standard

If you’re an expat, a GCC national, or a UAE citizen, you can apply. However, the FTA corporate looks closely at your physical presence.

- The 183-Day Rule: To be considered a tax resident, you must physically stay in the UAE for at least 183 days within a calendar year (or a consecutive 12-month period). Every partial day counts, even if you just land before midnight!

- Legal Standing: You must hold a valid residency visa and a current Emirates ID.

- Alternative Options: If you haven’t hit 183 days, you might still qualify under the 90-day rule if you have a permanent home (like an Ejari-registered apartment) and a local job or business.

For Companies: Proving Your Presence

Businesses can also secure a TRC to protect their global profits, but “paper companies” won’t make the cut.

- Incorporation & Licensing: Your company must be legally incorporated and hold a valid license (Mainland or Free Zone tax regulations) for at least one year.

- Financial Transparency: You must maintain proper accounting records. Most applications require audited financial statements or at least six months of certified bank statements to show the business is active.

- Management & Control: The FTA needs to see that the big decisions are made here. This means having a physical office; virtual offices are generally not accepted for TRC purposes.

Essentially, the criteria are there to show you are a real part of the UAE’s economy. If you meet these, you are ready to move on to the documentation stage.

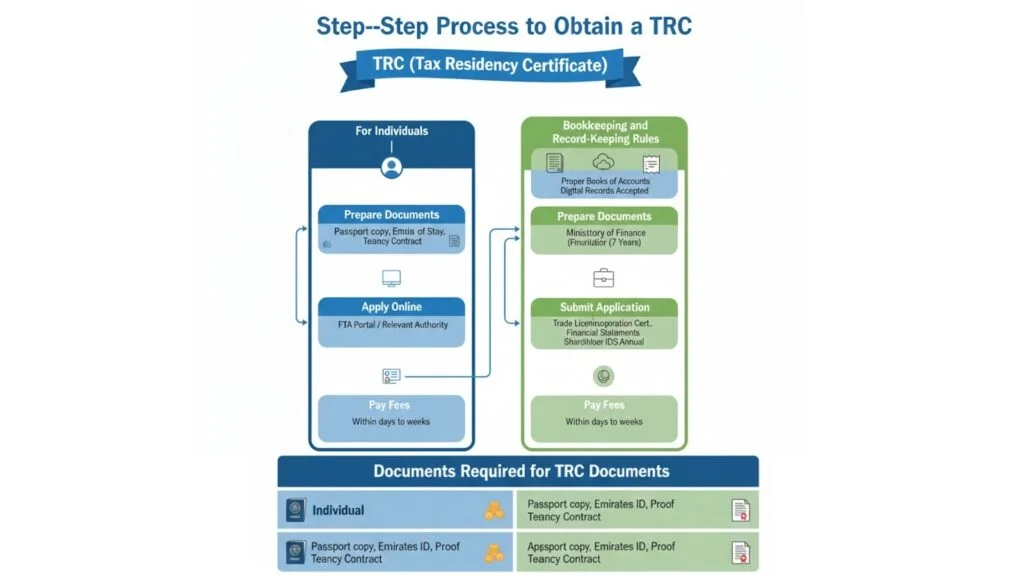

Step-by-Step Process to Obtain a TRC

Getting your certificate doesn’t have to be a headache. The UAE has moved the entire process online through the EmaraTax portal, making it faster and more transparent. Here is how you can get it done.

For Individuals: Securing Your Personal TRC

If you are an individual resident, the process is straightforward but requires attention to detail:

- Prepare Your Documents: Gather your passport, residency visa, Emirates ID, and a 6-month bank statement. You’ll also need your tenancy contract (Ejari) and an entry/exit report from the immigration department to prove you’ve spent enough time in the country.

- Apply Online: Head to the Federal Tax Authority (FTA) portal. Create a profile using your UAE Pass, select “Tax Residency Certificate,” and fill in the required details.

- Pay Upfront: As of late 2025, you generally pay the full fee at the time of submission. For individuals not registered for tax, this is usually around AED 1,000, plus a small AED 50 submission fee.

- Receive Your TRC: Once the FTA reviews your file (usually within 5–7 business days), you can download your digital certificate. If you need a physical stamped copy for a foreign government, you can request one for an extra AED 250.

For Companies: Proving Corporate Residency

The corporate path is slightly more rigorous to ensure the business is genuinely active in the UAE:

- Gather Corporate Records: You will need your trade license, Memorandum of Association (MOA), and audited financial statements. Don’t forget the passport and Emirates ID copies for shareholders and managers.

- Submit via EmaraTax: Log in to the business’s tax profile. Ensure you have your Corporate Tax TRN (Tax Registration Number) ready, as this is now mandatory for most applications.

- Pay the Fees: For companies not yet registered for corporate tax, the fee is approximately AED 1,750. If you are already a tax registrant, the fee is significantly lower, usually around AED 500.

- Download the Certificate: After a review period of about 7–12 working days, your certificate will be issued digitally.

Documents Required for TRC

| Applicant Type | Key Documents Required |

| Individual | Passport & Visa, Emirates ID, 6-month Bank Statement, Tenancy Contract (Ejari), Immigration Entry/Exit Report. |

| Company | Trade License, MOA, Audited Financial Statements, Shareholder IDs, 6-month Corporate Bank Statements. |

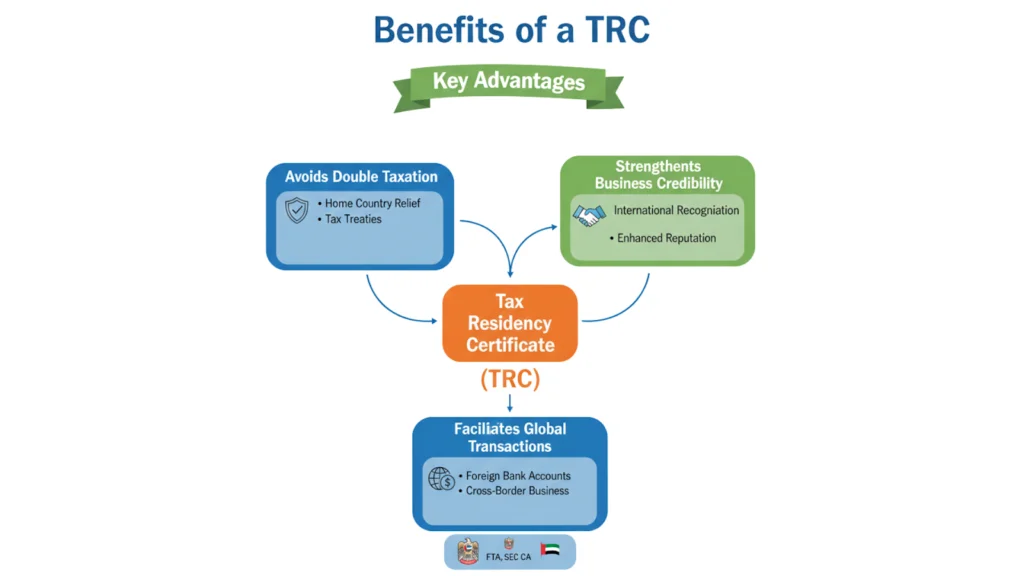

Benefits of a Tax Residency Certificate (TRC)

Why go through the effort of applying for a TRC? It’s not just about compliance; it’s about protecting your wealth and making your financial life significantly easier. Here are the three main reasons this document is a must-have:

1. Avoid Being Taxed Twice

The biggest win is the protection you get from Double Taxation Avoidance Agreements (DTAA). The UAE has a massive network of these treaties with over 130 countries.

When you hold a TRC, you have the legal proof needed to tell your home country (or any other country where you earn income) that you are already a tax resident in the UAE.

This can save you from paying double tax on dividends, interest, and royalties, keeping more money in your pocket.

2. Boost Your Global Credibility

In the eyes of international authorities and partners, a TRC is a badge of legitimacy. It shows that you aren’t just a “paper company” or a temporary visitor. For businesses, this is crucial when bidding for international contracts or working with global vendors.

It confirms that you are a serious entity, fully recognized by the UAE Federal Tax Authority, which builds trust and opens doors to higher-level partnerships.

3. Smarter Banking and Cross-Border Moves

If you’ve ever tried to open a foreign bank account or send a large sum of money across borders, you know the scrutiny involved. Banks are more cautious than ever about money laundering and tax evasion.

- Easier Approvals: Presenting a TRC clarifies your tax status immediately, often speeding up the process for opening accounts abroad.

- Reduced Withholding Tax: For businesses, a TRC can trigger lower withholding tax rates at the source, meaning you get your payments faster and with fewer deductions.

Essentially, the TRC acts as a “financial passport,” ensuring your transactions flow smoothly without getting stuck in red tape or extra fees.

Common Challenges When Applying for a TRC

While the process is digital and efficient, it isn’t always a walk in the park. Small mistakes can lead to big delays or even a rejected application.

Since the UAE updated its rules in late 2025, the stakes are higher because application fees are now often non-refundable.

1. Missing or Incorrect Documents

The most frequent hurdle is simply not having the right paperwork in the right format. Common slip-ups include:

- Incomplete Bank Statements: Providing only a few months instead of the full six-month history required.

- Expired Ejari: Using a tenancy contract that has lapsed or isn’t properly registered with the authorities.

- Mismatched Info: Ensuring the name on your trade license, bank account, and utility bills matches perfectly. Even a small typo can trigger a “request for more information,” pushing your timeline back by weeks.

2. Falling Short of Residency Rules

Many people assume that simply having a residency visa is enough. However, the Federal Tax Authority (FTA) looks at your actual physical presence.

- The Day Count: If you haven’t hit the 183-day mark (or the 90-day mark with a permanent home and job), your application will likely be denied.

- Travel Logs: Applicants often forget to include a clear “Entry/Exit Report” from the immigration department, which is the only proof the FTA accepts for your time spent in the country.

3. Delays and Portal Glitches

With the rollout of the EmaraTax portal updates for 2026, some users experience technical hiccups.

- TRN Confusion: A common challenge for businesses is selecting the wrong Tax Registration Number (TRN) during the start of the application. If you select your Corporate Tax TRN instead of your VAT TRN (if you have one), the system might show an “ineligible” error or apply a higher fee.

- Government Processing Times: While the standard turnaround is 5–10 business days, peak seasons (like the end of the financial year) can see these timelines stretch as the authorities deal with a high volume of requests.

Who to Consult for a Tax Residency Certificate in the UAE

If you want to skip the confusion and ensure your application is handled the first time correctly, getting professional advice is the smartest move. You can turn to HFA Consulting, a team of experts dedicated to making the entire process effortless for both individuals and businesses.

As experienced tax consultants in Dubai, they understand the fine print of the 183-day rule and the latest FTA portal updates for 2026. By letting them audit your documents and manage your submission, you save valuable time and significantly reduce the risk of a rejected application, giving you the peace of mind that your tax status is fully protected.

Conclusion

Securing a Tax Residency Certificate is an essential move for anyone living in the UAE or planning to open a Business in Dubai with international ties. It is the most effective way to protect your global earnings from being taxed twice while building instant credibility with foreign authorities and banks.

By following the correct steps from verifying your 183-day stay to ensuring your documents are crisp and up to date, you can enjoy a smooth application process through the EmaraTax portal.

Remember, maintaining accurate financial records and staying on top of your residency requirements are the keys to a quick approval. Strong financial discipline, including proper basic bookkeeping for small business practices, ensures your records are always ready for review and fully compliant. With your TRC in hand, you can focus on growing your wealth and operations with the full confidence that your tax status is legally recognized and secure.

FAQs

Who is eligible to apply for a Tax Residency Certificate in the UAE?

Eligibility is open to both individuals and businesses. Individuals generally need to be physically present in the UAE for at least 183 days in a year, though you may qualify with 90 days if you have a permanent home and a local job. Companies must be incorporated in the UAE for at least one year and demonstrate that their “effective management” happens within the country.

How long does it take to get a Tax Residency Certificate?

The Federal Tax Authority (FTA) usually processes applications within 5 to 7 working days for individuals and 7 to 12 working days for companies. Once your documents are approved and the final fees are paid, your digital certificate is typically issued within a few additional days.

What documents are required to apply for a Tax Residency Certificate?

For individuals, you’ll need your passport, residency visa, Emirates ID, a 6-month bank statement, a registered tenancy contract (Ejari), and an official immigration report of your entry and exit dates. Companies are required to provide their trade license, Memorandum of Association, audited financial statements, and a physical office lease agreement.

Zeeshan Khan

My name is Zeeshan Khan, and I’m a UAE-based business and tax consulting professional with hands-on experience in VAT compliance, corporate tax advisory, business setup, and regulatory services. I work closely with startups, SMEs, and established companies to help them navigate UAE tax laws, improve compliance, and make informed financial decisions. With a strong understanding of FTA regulations, corporate structuring, and commercial taxation in the UAE, my focus is on translating complex laws into clear, practical guidance for business owners. Through my writing, I aim to provide accurate, up-to-date insights that help businesses stay compliant, reduce risk, and operate confidently in the UAE market.