Zeeshan Khan

Zeeshan Khan Feb 12, 2026

Feb 12, 2026

Table of Contents

Running a business in the UAE has always been about growth and opportunity. But with the recent introduction of federal taxes, there is a new layer of responsibility.

Have you checked if your business is fully compliant? If not, you might be sitting on a “tax time bomb” without even knowing it.

The UAE corporate tax penalty system is designed to ensure everyone plays by the rules. While the UAE remains a business-friendly hub, the Federal Tax Authority (FTA) is serious about deadlines and documentation.

Missing a registration date or filing an incorrect return isn’t just a minor slip-up; it can lead to heavy fines that eat into your hard-earned profits. Staying updated with the latest UAE tax news is no longer optional; it’s a survival skill for every business owner in 2026.

Overview of UAE Corporate Tax Penalties

In simple terms, a UAE corporate tax penalty is a fine charged by the government when a business fails to follow the tax rules.

Think of it like a “traffic ticket” for your company’s finances. If you miss a deadline, forget to register, or keep messy records, the authorities step in to ensure everything stays on track.

These penalties aren’t just for big corporations. Whether you are a small mainland company set up or a large entity in a free zone, these rules apply to you. This applies equally in a free zone vs mainland business structure comparison, as the compliance obligations remain the same.

Even if your UAE free zone business qualifies for a 0% tax rate, you are still required to register and file returns. Ignoring these administrative steps is often what triggers a surprise fine.

Who is Watching?

The Federal Tax Authority (FTA) is the official body in charge of managing and enforcing these rules. They aren’t just there to collect money; their goal is to make sure the UAE’s tax system is fair and transparent for everyone.

From conducting audits to issuing fine notices, the FTA Corporate Tax has the regulatory oversight to ensure every business, regardless of its size or location, is playing by the book.

Breakdown of Key Corporate Tax Penalties

Knowing the exact numbers can help you understand the stakes. Here are the most common fines currently enforced by the FTA:

| Violation Type | Penalty Amount (AED) | Frequency / Conditions |

| Late Registration | AED 10,000 | Fixed one-time penalty |

| Late Tax Returns | AED 500 | Per month (for the first 12 months) |

| Late Tax Returns (Long Term) | AED 1,000 | Per month (from the 13th month onwards) |

| Poor Record Keeping | AED 10,000 | Per violation (increases to AED 20,000 for repeats) |

| Non-Arabic Records | AED 5,000 | If records are not provided in Arabic upon request |

| Late Deregistration | AED 1,000 | Per month (capped at AED 10,000) |

| Late Payment of Tax | 14% Per Annum | Calculated monthly on the outstanding balance |

Staying compliant is the only way to protect your business from these unnecessary costs. Many of these fines, like the UAE corporate tax penalty for late registration, are applied automatically by the system, so there is no “wiggle room” once the deadline passes.

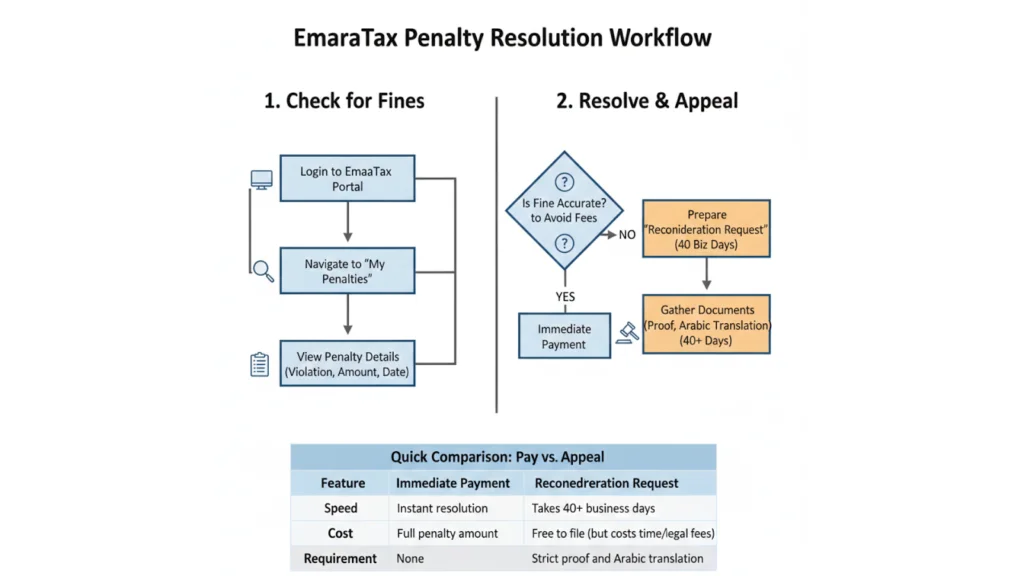

How to Check and Resolve Fines

If you suspect your business has been hit with a fine, don’t wait for a physical letter to arrive at your office. You can check your status instantly through the EmaraTax portal.

Simply log in, navigate to the “My Penalties” section, and you will see a clear list of any outstanding amounts along with the specific reasons behind them.

What if the fine is a mistake?

If you believe a fine was issued in error, you have the legal right to a corporation tax penalty appeal. You must submit a “Reconsideration Request” within 40 business days of the penalty notification.

Procrastinating here only makes things harder, as the FTA requires strict proof and documentation to waive any administrative charges.

Types of Corporate Tax Penalties in the UAE

Understanding the tax landscape is all about knowing where the “tripwires” are. The FTA has outlined several common corporate tax penalties that businesses may face if they fail to meet their obligations.

Here is a breakdown of the most frequent violations you should keep on your radar:

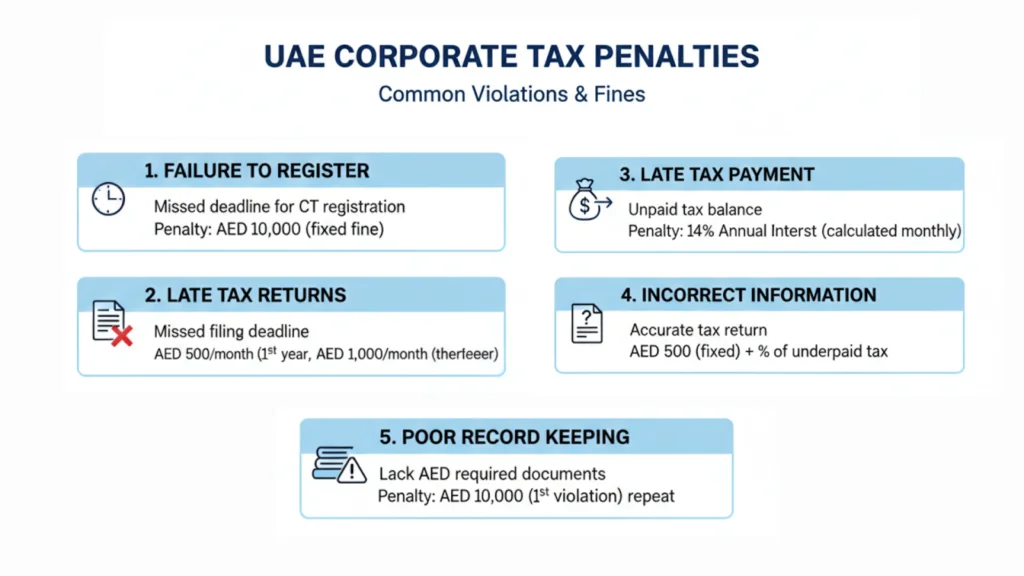

- Failure to Register for Corporate Tax: This is often the first hurdle. If you don’t submit your registration application within the FTA’s specified timeline, you face a fixed fine of AED 10,000.

- Late Submission of Corporate Tax Returns: Procrastination is expensive. Missing the filing deadline triggers a penalty of AED 500 per month for the first year, which doubles to AED 1,000 per month thereafter.

- Failure to Pay Corporate Tax on Time: If you file but forget to pay, the costs continue to climb. The FTA applies a 14% annual interest rate, calculated monthly, on any unpaid tax balance.

- Submission of Incorrect or Misleading Information: Accuracy is everything. Filing an inaccurate return can result in a fixed fine of AED 500. If the error leads to underpaid tax, much higher percentage-based penalties can be triggered.

- Failure to Maintain Required Records and Documentation: You must keep your receipts and ledgers in order. Failing to maintain proper records can cost you AED 10,000 per violation, rising to AED 20,000 for repeat offenses.

By staying organized and keeping a close eye on your deadlines, you can easily steer clear of these UAE corporate tax penalty traps.

Administrative Penalty Framework Under UAE Tax Law

The UAE has recently transitioned to a more refined and unified administrative penalty framework, primarily governed by Cabinet Decision No. 75 of 2023 and Cabinet Decision No. 129 of 2025. This revised structure represents a significant shift from a purely deterrent model to one focused on proportionality and compliance enablement.

By aligning the penalty logic across FTA Corporate Tax, VAT, and Excise Tax, the Federal Tax Authority (FTA) has created a cohesive procedural environment that reduces ambiguity for businesses operating across different tax categories.

Under this modern framework, penalties are strictly linked to the severity and duration of the non-compliance. For instance, the system distinguishes between fixed penalties, such as the one-time AED 10,000 fine for late registration, and percentage-based penalties that accumulate over time.

A key highlight of this evolution is the replacement of complex, compounding late-payment fees with a more predictable 14% annual interest rate, calculated monthly on unsettled balances.

This approach aligns the UAE’s tax enforcement with international standards, such as those recommended by the OECD, ensuring the global business community views the Emirates as a transparent and fair regulatory hub.

Late Registration & Filing Penalties

Missing a deadline might seem like a small mistake, but in the eyes of the FTA, it is a significant compliance gap. These failures are the most common ways businesses end up paying more than they should.

Here is what you need to know about the penalties for falling behind on your registration and filing:

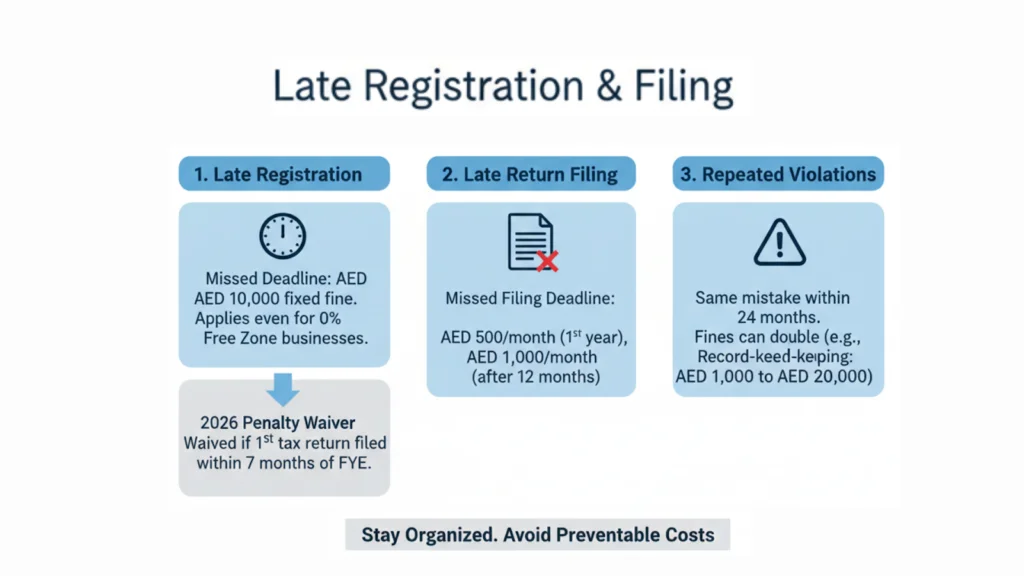

- Late Corporate Tax Registration: If you miss the deadline to register your business for corporate tax, you will face a fixed penalty of AED 10,000. This applies even if your business is currently loss-making or qualifies for a 0% rate in a free zone.

- Delayed Return Filing: Once you are registered, you must file your tax return every year. Failing to do so by the due date results in a monthly fine of AED 500 for the first year. If the return remains unfiled after 12 months, the fine jumps to AED 1,000 per month.

- Impact of Repeated Violations: The FTA keeps a digital “track record” of your compliance. Repeating the same mistake within 24 months, such as failing to keep records or making consistent filing errors, can see your fines double (e.g., from AED 10,000 to AED 20,000 for record-keeping breaches).

- Recent Penalty Relief & Waivers: There is some good news for those who act fast. The FTA has introduced a Penalty Waiver Initiative for 2026. If you were hit with the AED 10,000 late registration fine, you may have it waived or even refunded if you submit your first tax return within seven months of your financial year-end. This is a massive opportunity for SMEs to clean their slate.

By keeping a close eye on these dates, you can avoid these “preventable” costs and keep your business in the FTA’s good books.

Corporate Tax Penalties vs VAT Penalties

While both taxes are managed by the Federal Tax Authority (FTA), they function differently. For businesses already registered for VAT, the new corporate tax regime adds another layer of compliance. Understanding the boundary between these two is critical to avoid double fines. Many companies rely on VAT consultants in Dubai to navigate this complexity, ensuring proper adherence to both VAT vs corporate tax in the UAE.

Key Differences Between the Two Regimes

The main difference lies in what is being taxed. VAT is an indirect tax on transactions (sales and purchases), while Corporate Tax is a direct tax on your company’s net annual profit.

Because VAT is filed more frequently (usually quarterly), the opportunities for errors and penalties are higher. Corporate Tax, being an annual affair, has larger one-time penalties but fewer filing windows.

| Feature | Corporate Tax (CT) | Value Added Tax (VAT) |

| Tax Basis | Net Profit (Income) | Transaction Value (Consumption) |

| Filing Frequency | Annually | Monthly or Quarterly |

| Registration Fine | AED 10,000 (Fixed) | AED 10,000 (Fixed) |

| Late Filing Fine | AED 500 – AED 1,000 / month | AED 1,000 (first time) / AED 2,000 (repeat) |

| Late Payment Interest | 14% Per Annum | 14% Per Annum (as of 2026) |

| Record Keeping | Annual Financial Statements | Transaction-level Invoices & Receipts |

Important Accounting Considerations

If your business is hit with a fine, you might wonder how it affects your books. Here are the key points to keep in mind:

- Nature of VAT Penalties: These are administrative costs. They often arise from simple mistakes like missing a TRN on an invoice or late submission of a return.

- Are VAT penalties allowable for corporation tax? No. Under UAE law, any administrative penalties or fines paid to a government entity are non-deductible. This means you cannot list these fines as an expense to reduce your taxable profit.

- The Compliance Overlap: For VAT-registered businesses, your VAT returns must reconcile with your annual financial statements used for Corporate Tax. Discrepancies between the two can trigger an FTA audit, potentially leading to penalties in both categories simultaneously.

- E-Invoicing Impact: Starting in 2026, the UAE is moving toward real-time digital invoicing. This means VAT errors may be spotted instantly, making it even more vital to have a clean accounting system before you file your Corporate Tax return.

Staying compliant in one area does not automatically mean you are safe in the other. Always ensure your tax agent is looking at the “big picture” of your total tax liability.

Can You Appeal a UAE Corporate Tax Penalty?

If your business receives a penalty notice, it isn’t necessarily the final word. Every taxpayer in the UAE has a legal right to challenge a UAE corporate tax penalty if they believe it was issued in error or if there are mitigating circumstances.

The FTA provides a structured dispute resolution process to ensure fairness and transparency.

When Is an Appeal Appropriate?

An appeal is generally appropriate if you can prove that the violation didn’t happen, or if a “force majeure” (unforeseeable) event prevented you from complying.

For example, if a technical glitch in the EmaraTax portal blocked your registration or if a serious medical emergency affected the person responsible for filing, you may have strong grounds for a challenge.

Here is what you need to know about the corporation tax penalty appeal process:

- Grounds for Appeal: You can challenge a fine based on factual errors (the FTA has the wrong data), technical issues (portal downtime), or exceptional circumstances that were beyond your control.

- Appeal Timelines and Deadlines: You must act quickly. The first step, a “Reconsideration Request,” must be submitted via the FTA portal within 40 business days of receiving the penalty notice. If you miss this window, the penalty is usually considered final and binding.

- Required Documentation: Evidence is the backbone of any appeal. You will need to provide the original penalty notice, detailed bank statements, correspondence with the FTA, and any supporting proof like “error” screenshots or official medical certificates in Arabic.

- Role of Tax Consultants: Navigating the legal language of the FTA can be daunting. Tax consultants play a vital role by reviewing your case, ensuring all documents are correctly translated into Arabic, and representing your business during TDRC (Tax Dispute Resolution Committee) hearings if the case escalates.

Taking the time to appeal a wrong fine not only saves you money but also keeps your company’s compliance record clean for future audits.

Consequences of Ignoring Corporate Tax Penalties

Choosing to ignore a UAE corporate tax penalty is a high-stakes gamble that rarely pays off for any business. The immediate impact is the rapid accumulation of debt; once a fine is issued, it doesn’t just sit there; it grows.

Under the current framework, unpaid taxes and administrative fines are subject to a 14% annual interest rate, which is calculated monthly.

This means a manageable fine can quickly spiral into a major liability that drains your company’s cash flow, making it harder to cover essential expenses like payroll or inventory.

Beyond the numbers, the reputational and regulatory risks are even more damaging. Being flagged by the Federal Tax Authority (FTA Corporate Tax Guide) for non-compliance puts your business under a microscope, making future audits more likely and more rigorous.

In a transparent market like the UAE, a history of tax violations can tarnish your brand’s credibility with banks, investors, and potential partners. Financial institutions may classify your business as “high-risk,” leading to difficulties in securing credit or renewing essential facilities.

The final stage of ignoring these obligations involves direct enforcement actions. The FTA has the authority to impose severe restrictions on businesses that consistently fail to meet their tax duties. This can range from the suspension of your tax certificates to the blocking of trade license renewals.

In extreme cases, repeated or deliberate non-compliance can lead to the blacklisting of business owners and directors, legal proceedings, or even the seizure of assets to settle outstanding debts.

Staying ahead of your tax obligations is not just about avoiding a fee; it is about protecting the very future of your enterprise in the Emirates.

How Businesses Can Avoid UAE Corporate Tax Penalties

Avoiding a UAE corporate tax penalty isn’t about luck; it is about building a solid compliance habit. The FTA values transparency and effort, so being proactive is your best defense.

Use this checklist to ensure your business stays on the right side of the law:

- Timely Registration and Return Filing: Never wait for the last minute. Most businesses must register based on their license issuance. For 2026, ensure you file your return within nine months from the end of your financial year to keep your record clean.

- Accurate Financial Records and Bookkeeping: The FTA requires you to maintain records for at least seven years. Use cloud-based accounting software like Zoho Books or Xero to track every dirham. Ensure your ledger is audit-ready with supported invoices and bank reconciliations.

- Regular Compliance Reviews: Schedule a “tax health check” every quarter. Review your taxable income against the AED 375,000 threshold and ensure that non-deductible expenses (like certain entertainment or fines) are correctly separated.

- Staying Updated with UAE Tax Law Changes: Tax regulations are evolving. For instance, the transition to digital e-invoicing in July 2026 will change how data is reported. Following reliable UAE tax news sources will help you adapt before new rules become mandatory.

- Engaging Professional Tax Advisors: Tax laws can be dense. A professional advisor ensures your calculations are 100% accurate, helps you navigate complex “Free Zone” exemptions, and can represent you if you ever need to file a corporation tax penalty appeal.

By treating tax compliance as a core part of your business strategy rather than a year-end chore, you protect your profits and your reputation.

Importance of Staying Updated With UAE Tax News

The tax landscape in the Emirates is evolving at a rapid pace, making it essential for business owners to keep their fingers on the pulse of UAE tax news. Regulatory updates are not just minor tweaks; they often redefine the very rules that govern your financial obligations.

For example, recent amendments like Federal Decree-Law No. 17 of 2025 have introduced major shifts in how the FTA handles audits and refunds, effective January 2026.

If your business is still following the “old way” of doing things, you could inadvertently trigger a UAE corporate tax penalty simply because you weren’t aware that a deadline had moved or a documentation requirement had changed. This is why preparing properly for a small business Audit in the UAE is essential to ensure your records, filings, and compliance processes are up to date.

Monitoring official FTA announcements is your first line of defense against unexpected fines. The authority regularly releases “Public Clarifications” and binding directions that help interpret complex laws.

Staying informed allows you to move from a “reactive” state, where you are constantly fixing errors after they happen, to a “proactive” compliance model.

Proactive businesses are the ones that adapt to changes like the 2026 e-invoicing mandate months before it becomes law, ensuring their systems are machine-readable and audit-ready.

By staying updated, you don’t just avoid penalties; you gain a strategic advantage by ensuring your cash flow isn’t suddenly disrupted by a preventable compliance crisis.

Which Corporate Tax Consultants in Dubai Can Help Avoid Penalties?

Choosing the right partner is the final step in securing your business’s financial health. While many firms offer basic accounting, specialized corporate tax consultants in Dubai, like HFA Consulting, go a step further by providing proactive risk mitigation and strategic planning.

These experts don’t just file your paperwork; they audit your internal processes to identify “fine triggers” before the FTA does. From ensuring your registration is submitted within the correct window to navigating complex transfer pricing rules, professional consultants act as a shield against the penalty of the UAE corporate tax system.

By outsourcing these high-stakes tasks to experienced professionals, you can focus on your core business operations with the confidence that your tax position is optimized, audit-ready, and 100% compliant with the latest federal laws.

Conclusion

The new tax era in the Emirates is all about being proactive. While the UAE corporate tax penalty system might seem strict, it is designed to keep the business environment fair, transparent, and aligned with global standards.

From avoiding late registration fines to preparing for the 2026 e-invoicing wave, staying informed is your greatest asset.

Ignoring these rules doesn’t just cost money; it puts your trade license and business reputation at risk. By keeping your books clean, marking your deadlines, and working with the right experts, you can turn tax compliance from a burden into a seamless part of your success story. Don’t wait for a notice to arrive; take control of your tax health today.

FAQS

What is the penalty for late Corporate Tax registration in the UAE?

If a business fails to register for Corporate Tax within the specific timeline set by the FTA, a fixed administrative penalty of AED 10,000 is imposed. This fine applies regardless of whether the business is currently profitable or has tax liabilities.

Can Corporate Tax penalties be waived?

Yes, under the 2026 Penalty Waiver Initiative, the FTA may waive or refund the AED 10,000 late registration fine. To qualify, a business must typically submit its first Corporate Tax return within seven months from the end of its first tax period.

Are VAT penalties deductible under Corporate Tax?

No. UAE law is very clear on this: any administrative fines or penalties paid to a government entity (including VAT or traffic fines) are non-deductible. You cannot use these costs to reduce your taxable profit when calculating Corporate Tax. If you want to calculate Corporate Tax in UAE, only allowable business expenses and deductions can be considered,so penalties or fines must be excluded from your calculations.

How long does a penalty appeal take in the UAE?

The first step of an appeal (the Reconsideration Request) must be submitted within 40 business days. The FTA typically responds within 45 business days of receiving the application. If the case moves to the Tax Dispute Resolution Committee (TDRC), the timeline can extend by several months depending on the complexity of the case.

Zeeshan Khan

My name is Zeeshan Khan, and I’m a UAE-based business and tax consulting professional with hands-on experience in VAT compliance, corporate tax advisory, business setup, and regulatory services. I work closely with startups, SMEs, and established companies to help them navigate UAE tax laws, improve compliance, and make informed financial decisions. With a strong understanding of FTA regulations, corporate structuring, and commercial taxation in the UAE, my focus is on translating complex laws into clear, practical guidance for business owners. Through my writing, I aim to provide accurate, up-to-date insights that help businesses stay compliant, reduce risk, and operate confidently in the UAE market.