Zeeshan Khan

Zeeshan Khan Mar 16, 2026

Mar 16, 2026

Table of Contents

For years, the UAE was celebrated as a tax-free haven, but the landscape has evolved into a sophisticated, world-class regulatory environment. As a business owner in 2026, you are no longer just managing a shop or a consultancy; you are navigating a dual-layered fiscal system where Corporate Tax vs VAT defines your financial strategy.

Understanding the difference between VAT and tax, specifically how an indirect consumption tax interacts with a direct tax on your bottom line, is the secret to maintaining a healthy cash flow and staying on the right side of the Federal Tax Authority (FTA).

The challenge isn’t just knowing that taxes exist; it’s mastering the nuances of compliance. While the VAT percentage in the UAE remains a steady 5%, the introduction of the 9% Corporate Tax has added a layer of complexity to reporting and record-keeping. Misinterpreting what VAT tax is in the UAE versus how profits are calculated for Corporate Tax can lead to expensive “mismatch” flags during audits.

Whether you are a startup hitting the mandatory registration threshold or an established firm optimizing for the new e-invoicing era, getting these fundamentals right is your first step toward long-term stability.

The difference between VAT and corporate tax in the UAE is that VAT is an indirect tax applied to goods and services, while corporate tax is a direct tax applied to business profits. VAT is paid by consumers but collected by businesses, whereas corporate tax is paid directly by companies on their net income.

Defining the Core: VAT vs. Corporate Tax

Understanding the fundamental difference between VAT and tax on your corporate profits is essential for any business operating in the Emirates. While they both contribute to the nation’s revenue, they function on entirely different ends of your financial statement. One is collected from your customers, while the other is calculated from your leftover earnings.

Because these tax systems operate differently, many companies seek guidance from an experienced tax consultant in Dubai to ensure their VAT reporting and corporate tax calculations remain compliant with UAE regulations.

What is VAT in the UAE?

To answer what VAT is in the UAE, simply: it is an indirect consumption tax. This means the burden of the tax ultimately falls on the final consumer, not the business itself. However, as a business owner, you play a critical role as a temporary custodian of these funds.

The Concept: VAT is levied at every stage of the supply chain. From the manufacturer to the wholesaler and finally the retailer, tax is added to the value created at each step.

The Role: Your business acts as a “collector” for the Federal Tax Authority (FTA). You collect the tax on your sales (Output VAT) and can often reclaim the tax you paid on business expenses (Input VAT) through professional VAT registration and TRN assistance.

The Rate: The standard UAE VAT percentage is currently fixed at 5%. While this is one of the lowest rates globally, the compliance requirements for documentation and filing are strict.

VAT Rate in UAE

The standard Value Added Tax (VAT) rate in the UAE is 5%, a rate applied to the vast majority of goods and services supplied within the country. While some sectors are classified as zero-rated or exempt, the 5% standard remains the baseline for most commercial activities.

The following table provides a clear breakdown of the standard rate applicable to your business operations:

| VAT Type | Rate |

| Standard VAT rate | 5% |

At its core, the mechanism of this tax is straightforward for the business owner. It is an amount charged directly to customers at the point of sale, over and above the price of your goods or services.

Because the business acts as an intermediary, this tax is collected by businesses from their clients during daily transactions. Ultimately, the funds collected are not revenue for the company; they must be periodically paid to the Federal Tax Authority (FTA) through your regular tax filings.

Who Must Register for VAT in the UAE

Determining whether your business requires VAT registration is a critical compliance task based on your taxable turnover. The Federal Tax Authority (FTA) defines two specific benchmarks to manage this process.

Mandatory Registration Threshold

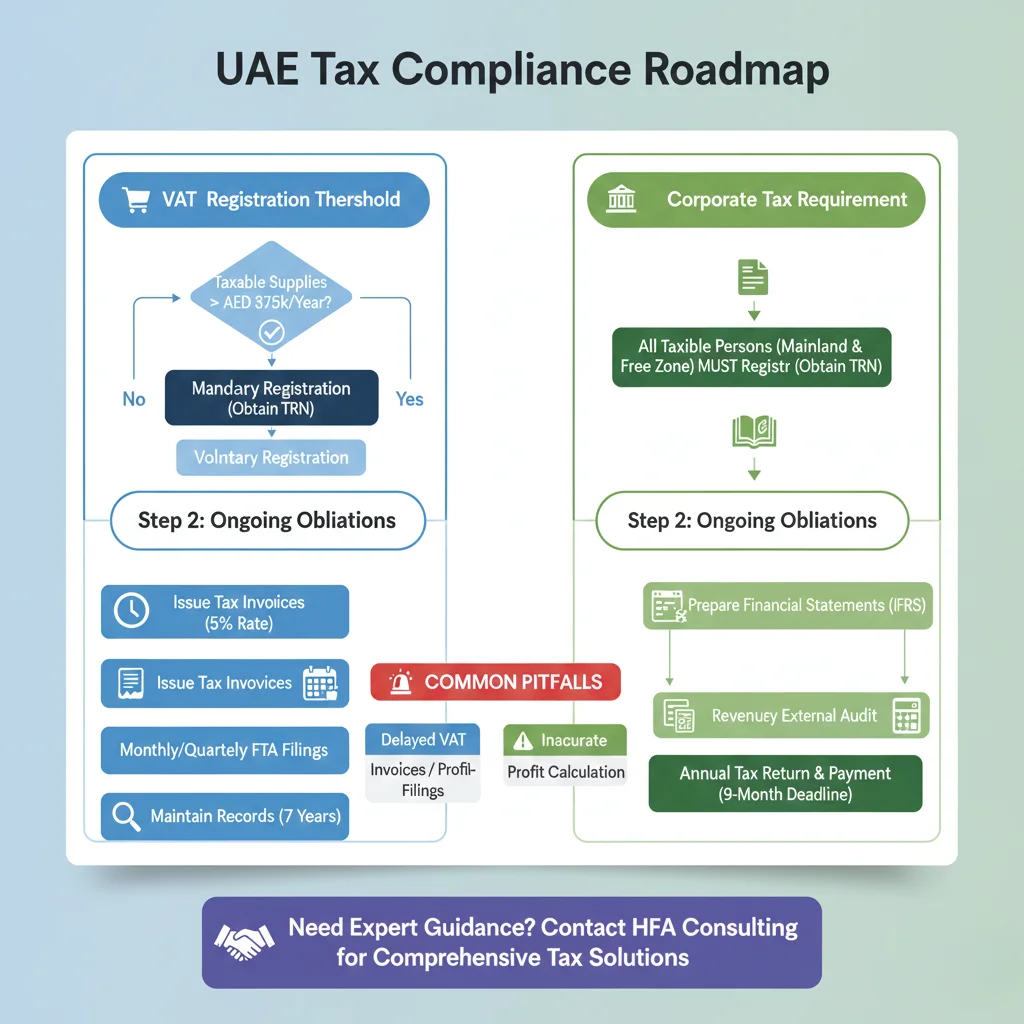

Registration is legally required if your taxable supplies and imports in the UAE exceed AED 375,000 over the previous 12 months. You must also register if you have reasonable grounds to anticipate that your taxable supplies and imports will surpass this AED 375,000 threshold within the next 30 days. Failure to register within the mandated timeframe can result in significant administrative penalties.

Voluntary Registration Threshold

Businesses that do not meet the mandatory criteria may choose to register voluntarily if their taxable supplies, imports, or taxable expenses exceed AED 187,500.

While optional, this is a strategic choice for startups and growing companies; it allows businesses to reclaim input VAT on initial setup costs and often enhances professional credibility when dealing with corporate clients and suppliers.

What is Corporate Tax in the UAE?

When asking what Corporate Tax is in the UAE, you are looking at a direct tax. Unlike VAT, which is external to your profit margins, Corporate Tax is a direct levy on the wealth your company generates.

The Concept: This tax is imposed on the “net accounting profit” of a business. It is calculated after all your allowable business expenses, such as salaries and rent, have been deducted from your total revenue.

The Role: This is a direct cost to the business. You cannot “charge” your customers an extra 9% on their invoice to cover your Corporate Tax; it must be paid out of the company’s actual profits.

The Rate: The UAE follows a tiered system to support small businesses and startups. You pay 0% on taxable profits up to AED 375,000. Any profit exceeding that threshold is subject to a 9% tax rate.

Staying compliant with this requires diligent Bookkeeping and Accounting Best Practices to ensure your profit declarations are accurate and audit-ready.

Strategic Comparison: The Fundamental Differences

Navigating the VAT and tax difference requires more than just knowing the definitions; it requires a strategic understanding of how these two systems impact your daily operations and year-end evaluations. While they coexist, their influence on your financial health originates from different sources.

The primary difference between VAT and tax on corporate earnings lies in the “taxable base.” VAT is calculated on the gross value of your sales, essentially your top-line revenue. In contrast, Corporate Tax is focused on your “bottom line,” or what is left over after you have accounted for all operational costs and deductible expenses.

Comparison Overview: VAT vs. Corporate Tax

The table below highlights the core differences

| Feature | VAT (Value Added Tax) | Corporate Tax |

| Tax Base | Total Sales / Revenue | Net Accounting Profit |

| Standard Rate | 5% | 9% (on profits above AED 375,000) |

| Who Pays? | The End Consumer | The Business / Shareholders |

| Filing Frequency | Monthly or Quarterly | Annually |

| Financial Focus | Transactional | Periodical / Annual |

Incidence and Economic Burden

When managing VAT in Dubai, businesses often feel the pressure of collection, but it is important to remember that the economic burden rests with the consumer. You are simply the intermediary passing that 5% to the government. Corporate Tax, however, is an inescapable cost for shareholders.

It directly reduces the distributable dividends and retained earnings of the company, making a Mandatory UAE Corporate Tax Guide essential for long-term fiscal planning.

Reporting Frequency and Compliance

The administrative rhythm of these two taxes varies significantly. VAT Tax Dubai compliance is a high-frequency task, often requiring monthly or quarterly returns depending on your annual turnover.

This keeps the FTA updated on your transactional volume in real-time. On the other hand, Corporate Tax is an annual obligation, requiring a comprehensive look at your fiscal year’s performance.

Accounting and Balance Sheet Impact

From an accounting perspective, VAT is largely a balance sheet item. The money you collect is a “liability” (owed to the FTA), and the VAT you pay to suppliers is an “asset” (receivable/offset). It doesn’t typically touch your profit and loss statement unless you cannot recover it.

Corporate Tax is the opposite; it appears directly on your income statement as a tax expense, reducing your net income. To manage these complexities effectively, many firms rely on Comprehensive UAE Payroll Outsourcing Services and dedicated accounting teams to ensure that salary-related deductions and tax provisions are handled accurately

How VAT and Corporate Tax Work Together

While many businesses view VAT and Corporate Tax as separate administrative burdens, they are fundamentally different mechanisms that operate simultaneously within your financial ecosystem.

It is a common misconception that these two taxes overlap; in reality, they target entirely different stages of your business’s financial lifecycle.

Distinct Tax Bases: Transactions vs. Profits

The most important distinction is what the tax is actually levied upon. VAT applies strictly to the transactional level. Every time you sell a product or service, VAT is triggered as an indirect consumption tax.

It is a tax on the movement of goods and services, meaning it is detached from your actual financial performance. You collect this on behalf of the government, regardless of whether your business is currently running at a loss or a profit.

Conversely, Corporate Tax applies to your net accounting profit. This is a direct tax on the wealth your company has generated after subtracting all allowable operational expenses, such as rent, salaries, and cost of goods sold.

While VAT is a high-frequency, transactional obligation, Corporate Tax is a performance-based, periodical evaluation of your business’s bottom line.

A Practical Example of Dual Compliance

To understand how these operate concurrently, consider a business selling electronic goods. During the year, the business performs two distinct tax functions:

- VAT Collection: When the business sells a product for AED 1,000, it must charge the customer an additional 5% VAT (AED 50). This AED 50 is not income; it is a liability collected from the customer that must be remitted to the Federal Tax Authority (FTA).

- Corporate Tax Calculation: At the end of the financial year, the business looks at its total revenue minus all expenses. If the business made a net profit exceeding the threshold of AED 375,000, it must pay 9% Corporate Tax on that specific profit figure.

Both taxes function independently but simultaneously. You are responsible for managing the “flow” of VAT on a daily, monthly, or quarterly basis, while simultaneously maintaining the financial records required to calculate your “bottom line” profit for the annual Corporate Tax filing.

The distinction between these two views, VAT as a movement of cash through your accounts and Corporate Tax as a final assessment of your earnings, is the hallmark of a fiscally healthy UAE enterprise.

Compliance Roadmap for UAE Entities

Staying compliant in the UAE’s evolving tax environment requires a proactive approach. It is no longer enough to simply “do the books” at the end of the year; businesses must align their internal processes with specific regulatory milestones to avoid heavy administrative penalties.

Businesses often rely on professional tax consultancy services in Dubai to manage VAT filings, corporate tax registration, and financial reporting requirements.

Registration Thresholds

Understanding when to register is the first hurdle. For VAT, the criteria are based on your transaction volume, while Corporate Tax registration is almost universal for legal entities.

VAT Registration: This becomes mandatory once your taxable supplies and imports exceed AED 375,000 over the previous 12 months or are expected to exceed that amount in the next 30 days.

Many startups also opt for voluntary registration at the AED 187,500 mark to reclaim input tax on their initial setup costs.

Corporate Tax Registration: Unlike VAT, there is no “earnings threshold” for registration. What is Corporate Tax in the UAE? Compliance starts with the requirement that all taxable persons, including mainland companies and Free Zone entities, must register and obtain a Tax Registration Number (TRN), regardless of whether they are currently profitable.

Record-Keeping and Documentation

The quality of your documentation is what will protect you during an audit. The FTA has set high standards for how financial data should be captured and stored.

VAT Invoicing: In the UAE, you are required to issue a compliant tax invoice within 14 days of a supply. With the rollout of mandatory e-invoicing starting in 2026 for many sectors, these invoices must now be structured digitally.

Failing to meet these strict timelines or formatting requirements is one of the quickest ways to trigger a review, making it vital to understand how to handle FTA VAT Audits before they happen.

Financial Statements: For Corporate Tax purposes, the FTA generally requires that taxable income be determined based on standalone financial statements. Larger businesses (with revenue exceeding AED 50 million) and Qualifying Free Zone Persons are specifically mandated to prepare audited financial statements according to International Financial Reporting Standards (IFRS).

Even if an audit isn’t mandatory for your specific turnover, maintaining records that meet these standards is a best practice for total transparency.

Results and Business Impact Expectations

The interplay between VAT vs. Corporate Tax is not just a matter of compliance; it is a fundamental driver of your business strategy in the UAE.

As these regulations mature, they influence everything from how you price your products to how you manage your internal operations, including WPS Compliance and Management in Dubai, to ensure labor costs are accurately reflected in your tax filings.

Pricing Strategy and Market Competitiveness

While the VAT percentage in the UAE is relatively low compared to the global average, its impact on consumer behavior is real. Because VAT is an “add-on” at the point of sale, businesses must decide whether to absorb the cost to stay competitive or pass it entirely to the customer.

In a price-sensitive market, even a 5% difference can influence a buyer’s decision. Companies must analyze their margins carefully to ensure that their “tax-inclusive” pricing remains attractive without eroding the profits intended for shareholders.

Profitability Management and Optimization

Corporate Tax has turned the spotlight onto “deductible expenses.” To optimize the 9% liability, businesses are becoming more disciplined about documenting every legitimate operational cost.

From marketing spend to employee benefits, ensuring every expense is “wholly and exclusively” for business purposes is key.

This shift encourages more rigorous financial planning, as companies seek to reinvest profits into growth areas that simultaneously serve as tax-efficient deductions.

Cash Flow Dynamics

Perhaps the most significant impact is on a company’s liquidity. VAT creates a high-frequency cash flow cycle: you collect it daily and remit it to the government monthly or quarterly.

This requires a robust system to ensure you aren’t accidentally spending “tax money” on operations. Corporate Tax, by contrast, is a looming year-end obligation.

Managing the transition between these two, balancing the immediate “in-and-out” of VAT against the long-term “set-aside” for Corporate Tax, is the hallmark of a sophisticated UAE enterprise.

Common Misconceptions About VAT and Corporate Tax

As the UAE’s regulatory landscape matures, several myths have emerged that can lead businesses and individuals into avoidable compliance traps. Clarifying these misunderstandings is essential for maintaining a healthy relationship with the Federal Tax Authority (FTA).

VAT and Corporate Tax Are the Same

A prevalent, yet dangerous, misconception is that VAT and Corporate Tax are interchangeable or that being compliant with one automatically satisfies the requirements of the other. In reality, they are completely distinct.

VAT is an indirect consumption tax levied on the transaction of goods and services, collected by businesses on behalf of the government. Corporate Tax, however, is a direct tax levied on the net profit of a business entity.

They operate on different financial bases, VAT on revenue and Corporate Tax on profit, and involve separate registration, filing, and calculation processes.

Only Large Companies Pay Corporate Tax

Many small business owners and startups incorrectly assume that Corporate Tax is only a concern for large corporations. The UAE Corporate Tax regime applies to a broad range of entities, including small and medium-sized enterprises (SMEs).

While the UAE provides a 0% tax rate on taxable profits up to AED 375,000 to support smaller businesses, the requirement to register, maintain proper financial records, and file annual tax returns remains mandatory for most taxable persons, regardless of their size or total profit.

Freelancers Don’t Need Corporate Tax Registration

There is a common belief that because freelancing is an individual activity, it falls outside the scope of Corporate Tax. This is incorrect. If you operate as a freelancer with a license, or if your business activities generate an annual turnover exceeding AED 1 million, you are considered a “taxable person” under UAE law.

While your personal salary or passive investment income remains exempt, your freelance business income is subject to the same regulatory oversight as formal companies.

Ignoring registration requirements because you are a “solo” operator can lead to significant administrative penalties, making it vital to monitor your annual turnover closely.

When Businesses Need Professional Tax Advice

As the UAE’s regulatory framework continues to evolve, the distinction between transactional compliance and annual profit reporting has become increasingly sophisticated.

While many business owners manage initial setup on their own, the growing complexity of tax compliance often necessitates professional intervention.

Many companies prefer working with a professional tax consultant in Dubai to ensure they remain compliant with both VAT and corporate tax regulations, effectively mitigating the risk of inadvertent errors and costly penalties.

Compliance Complexity

The administrative burden of managing two simultaneous tax regimes is significant. VAT requires frequent, high-volume transactional reporting, while Corporate Tax demands detailed annual financial audits and precise expense categorization.

As your business scales, the risk of “mismatch” flags between your VAT returns and your profit declarations increases. A professional consultant provides the necessary oversight to align these disparate reporting requirements, ensuring that your financial data is audit-ready and accurate at all times.

Adapting to Changing Tax Regulations

The UAE’s tax landscape is dynamic, with new guidelines, e-invoicing mandates, and threshold adjustments being introduced regularly. Staying updated on these shifting requirements while running daily operations is a challenge for any leadership team.

Professional tax advisors not only track these legislative updates but also translate them into actionable operational strategies. By proactively adjusting your internal bookkeeping and tax-planning processes, you can stay ahead of regulatory changes rather than reacting to them after an audit notification.

Conclusion

Piloting the nuances of corporation tax vs vat is no longer just a task for the accounting department; it is a core pillar of executive strategy. Understanding that VAT is focused on the transactional flow of goods and services, while Corporate Tax evaluates the actual profitability of your enterprise, is vital for the long-term success of any UAE-based business.

By mastering the difference between VAT and tax applications, you protect your company from the risks of non-compliance and ensure that your financial health remains robust in a competitive, regulated market.

As the UAE tax landscape matures, the most visionary step a business owner can take is to move away from siloed reporting. Integrating these two systems into a single, digital accounting framework allows for real-time visibility into both your consumption tax obligations and your profit tax liabilities.

Working with a qualified tax advisor in Dubai can help businesses navigate both VAT compliance and corporate tax obligations more efficiently.

Whether you are managing a small consultancy or a large industrial firm, staying informed and proactive is your best defense against administrative hurdles.

FAQs

Can a business be registered for both VAT and Corporate Tax in the UAE?

Yes, many businesses in the UAE are required to comply with both VAT and Corporate Tax. VAT applies to the supply of goods and services once the registration threshold is met, while Corporate Tax is assessed on taxable profits. If a business meets the conditions for both regimes, it must register, file returns, and comply with each separately.

Is VAT calculated on profit in the UAE?

No, VAT is not calculated on profit. It is charged on the value of taxable goods and services sold, regardless of whether the business is making a profit or a loss. This is why businesses must continue VAT compliance even during low-profit or loss-making periods.

Are Free Zone companies exempt from both VAT and Corporate Tax in the UAE?

Free Zone companies are generally subject to VAT if they make taxable supplies in the UAE. For Corporate Tax, Free Zone entities may benefit from a 0% Corporate Tax rate if they qualify as a Qualifying Person and meet all regulatory conditions set by the UAE authorities. Compliance requirements still apply even when the 0% rate is available.

Zeeshan Khan

My name is Zeeshan Khan, and I’m a UAE-based business and tax consulting professional with hands-on experience in VAT compliance, corporate tax advisory, business setup, and regulatory services. I work closely with startups, SMEs, and established companies to help them navigate UAE tax laws, improve compliance, and make informed financial decisions. With a strong understanding of FTA regulations, corporate structuring, and commercial taxation in the UAE, my focus is on translating complex laws into clear, practical guidance for business owners. Through my writing, I aim to provide accurate, up-to-date insights that help businesses stay compliant, reduce risk, and operate confidently in the UAE market.