Muhammad Saad

Accountant

Zeeshan Khan

Client Accounting Manager

Managing a company is demanding enough without the added weight of ever-changing tax codes. For many business owners, the "tax season" isn't just a few weeks in spring; it is a year-round source of anxiety. Between staying compliant with federal regulations and managing state-level obligations, the margin for error is razor-thin.

Without professional tax consultancy, even the most organised founders can find themselves buried under paperwork and conflicting advice. The complexity isn't just about the math; it is about understanding the legal nuances that apply to your specific industry.

Timing is everything when it comes to tax compliance. A single missed date for estimated payments or an extension request can trigger a chain reaction of interest charges and late-filing fees. These penalties aren't just one-time costs; they erode cash flow and can increase the likelihood of future scrutiny. When day-to-day operations take priority, tracking the exact tax deadline for your entity type often slips until a notice arrives.

Not all businesses are taxed the same way. Whether you operate as an LLC, S-Corp, or C-Corp, each structure carries distinct obligations and benefits. The confusion often starts with choosing the right form, such as Form 1120 for corporations or Form 1065 for partnerships. Many companies overpay simply because they don't know which deductions they qualify for or how to treat multi-state income. This lack of clarity often leads to a "guesswork" approach that can result in penalties or missed opportunities.

Accuracy is the bedrock of a clean return. Small discrepancies between your bookkeeping and your tax filings can trigger a Tax Penalty or, worse, a full-scale audit. Inconsistent documentation or "messy" books make it impossible to prove your expenses during a review. Without a clear system to track credits and liabilities, your financial reporting becomes a liability rather than a tool for growth.

We provide an end-to-end compliance ecosystem designed to protect your company's financial health. Rather than just filing forms once a year, our team acts as a strategic partner in your growth. As part of our broader corporate tax services, we handle the heavy lifting of regulatory paperwork so you can stay focused on your core. Our approach is bespoke to your specific business structure, whether you are a single-member LLC, a growing S-Corp, or a complex C-Corp with multi-state operations.

Compliance begins before the first dollar is earned. We assist new and expanding businesses in securing the necessary tax identifications and ensuring you are registered with the appropriate federal and state authorities. Setting up your tax profile correctly from day one prevents "mismatch" errors that often lead to future delays or rejected filings.

This is the core of our annual commitment to your business. We take a thorough approach to Corporate Income Tax Filing, ensuring every deduction is captured and every credit is applied. Our experts handle the preparation and electronic submission of Form 1120 (for C-Corps) and Form 1120-S (for S-Corps), verifying that your taxable income is reported with 100% accuracy to minimise your overall liability.

Tax strategy shouldn't be reactive. We provide year-round advisory to help you understand how business decisions like hiring new employees or purchasing equipment impact your tax position. By managing your Estimated Tax Payments throughout the year, we ensure you aren't hit with a massive, unexpected bill or underpayment penalties during the filing season.

The word "audit" shouldn't cause panic. We offer powerful Audit Representation to stand by your side if state authorities request a review of your books. Our team handles the communication, organizes the necessary documentation, and defends your filings. We act as your professional shield, ensuring that your rights are protected and that the process is resolved as quickly as possible.

Under the current UAE Corporate Tax Law, the regulatory prospect has shifted from a tax-free environment to a structured compliance regime. It is no longer optional for businesses to maintain tax records; filing an annual return is now a foundational legal requirement for almost all entities operating within the Emirates. Whether you are a startup in Dubai or an established firm in Abu Dhabi, understanding your specific obligations is the only way to safeguard your business from high-stakes enforcement actions.

According to Federal Decree-Law No. 47 of 2022, every taxable person, including mainland companies and individuals conducting business activities, must file a corporate tax return for each tax period.

A common misconception is that Free Zone entities are exempt from documentation. Even if your business qualifies for a 0% Corporate Tax rate as a Qualifying Free Zone Person (QFZP), you are still legally required to register with the FTA and submit a full tax return annually.

Precision is vital. Businesses must file their return and settle any payable tax within nine months from the end of their relevant financial year. For example, if your financial year ended on December 31, 2025, your filing must be completed by September 30, 2026.

The Federal Tax Authority (FTA) has moved toward more strict enforcement. Non-compliance, including late registration or failure to file on time, now triggers significant financial consequences:

| Offence | Penalty |

| Late Registration | Flat penalty of AED 10,000 |

| Late Filing | AED 500/month for first 12 months, then AED 1,000/month |

| Late Payment | 14% annualised interest rate, accrued monthly |

While government entities, extractive businesses, and certain public benefit organisations may be exempt, they must still meet specific notification requirements. Most private commercial enterprises are classified as taxable businesses and must adhere to the standard 9% rate on taxable income exceeding AED 375,000.

Filing a return is only half the battle; ensuring its accuracy and timeliness is what protects your company's standing. Local authorities, like the FTA, operate on a system of strict accountability. When a business fails to meet these standards, the consequences are rarely just administrative; they are financial and operational.

The most visible impact of a filing error is the immediate hit to your cash flow. Penalties are typically structured as follows:

| Risk Category | Financial Consequence (2026 Standards) |

| Failure-to-File | An immediate monthly penalty of AED 500 for the first 12 months, escalating to AED 1,000 per month thereafter. This applies even for "Nil" returns. |

| Failure-to-Pay | A monthly penalty calculated at an annualised rate of 14% is applied to any outstanding tax balance from the day following the due date until the debt is cleared. |

| Compounding Interest | Tax interest compounds over time, meaning even a small initial oversight can grow into a significant liability over 6–12 months. |

| Late Registration | A fixed administrative penalty of AED 10,000 is imposed on businesses that fail to submit their registration via EmaraTax within prescribed timelines. |

Consistent filing errors or late submissions flag your business as "High Risk" in regulatory databases, potentially leading to:

| Risk Category | Long-Term Business Impact |

| Loss of Good Standing | Non-compliance can result in suspension of your trade license or eligibility for government tenders. A Tax Clearance Certificate is required for many B2B/B2G contracts. |

| Credit & Finance Impact | Outstanding liabilities and penalties are reported to the Al Etihad Credit Bureau, negatively affecting your corporate credit score and financing options. |

| Operational Restrictions | The FTA can block transactions on EmaraTax for non-compliant entities, preventing VAT invoicing or business modifications until issues are resolved. |

| Extended Audit Window | If "Tax Evasion" or "Failure to Register" is suspected, the statute of limitations for an audit can extend from 5 years to 15 years. |

Audits are often triggered by certain red flags in a tax return:

| Audit Trigger | Regulatory Risk & Technical Indicator |

| Mismatched Data | Income on your Corporate Tax Return not aligning with VAT returns or third-party data triggers automated flags. |

| Unusually High Deductions | Claiming business expenses above industry benchmarks often prompts a verification request. |

| Rounded Numbers | Expenses reported in perfectly round numbers (e.g., AED 500 or 1,000) suggest estimation instead of exact accounting. |

| Inconsistent Reporting | Failing to align multi-jurisdictional filings with federal totals can trigger cross-border investigations. |

Filing a corporate tax return is a data-driven process that requires absolute synchronisation between your accounting records and the UAE Corporate Tax Law. The Federal Tax Authority (FTA) expects a high level of transparency and digital accuracy. To ensure your submission is processed without delays or inquiries, your business must maintain a comprehensive compliance file that satisfies Federal Decree-Law No. 47.

This is the bedrock of your filing. You must provide a complete set of financial statements, including your Balance Sheet, Profit and Loss (P&L) statement, and Cash Flow report. For 2026 compliance, the FTA requires these to be prepared according to IFRS (International Financial Reporting Standards). Maintaining these records digitally is essential, as the authority may request them during a desk audit to verify your taxable income.

You cannot file a return without a valid Tax Registration Number (TRN). Your corporate tax registration must accurately reflect your current trade license, business activity, and ownership structure. If you have recently changed your business address or added a new branch, these details must be updated on the EmaraTax portal before you attempt to submit your annual filing.

Every figure on your return must be defensible. Under the Tax Procedures Law, you are required to maintain a systematic record of:

| Documentation Category | Purpose & Regulatory Requirement |

| Sales Invoices & Revenue Logs | Mandatory to verify your Gross Income and ensure all taxable revenue streams are captured. |

| Expense Receipts | Serves as the primary evidence for all deductible business expenses to ensure tax-deductible claims are valid. |

| Bank Reconciliation Reports | Critical proof that your reported "on-paper" profit matches your actual cash movement and bank balances. |

| Related Party Records | Detailed logs of intra-group dealings, which must prove "Arm’s Length" pricing to comply with Transfer Pricing rules. |

Depending on your entity type, whether you are a Mainland Business, an LLC, or a Qualifying Free Zone Person, you must submit specific forms via the FTA portal. Remember the "9-Month Rule": your return and any applicable tax payment must be submitted within nine months of your financial year-end. Failing to align your filing with this specific window triggers an immediate late-filing penalty.

While every registered entity has a legal obligation to file, certain business structures carry a higher risk of error due to their operational complexity. In the current 2026 regulatory environment, "doing it yourself" often costs more in penalties than the price of professional oversight.

For SMEs, cash flow is the lifeline of the business. Professional filing ensures that you aren't overpaying on your taxable income and that every eligible deduction is claimed. We help small business owners move away from "shoebox accounting" toward a structured system that satisfies the Federal Tax Authority (FTA).

Limited Liability Companies and larger Corporations often deal with inter-company loans, shareholder distributions, and varied asset depreciations. These elements require sophisticated reporting. If you operate as an LLC, S-Corp, or C-Corp, professional support is vital to ensure your Form 1120 or local equivalent aligns perfectly with your corporate bylaws.

The 2026 rules for Free Zones are strict. Even if you qualify for a 0% Corporate Tax rate, you must still meet "Substance Requirements" and file an annual return. We help Free Zone entities maintain their "Qualifying" status, ensuring they don't accidentally slip into the 9% taxable bracket due to a filing technicality.

Mainland companies face the standard 9% UAE Corporate Tax on profits exceeding AED 375,000. Because mainland entities often engage in diverse local and international trade, their bookkeeping requires precise VAT-to-Corporate Tax reconciliation to avoid automated audit triggers.

Digital entrepreneurs and e-commerce platforms often struggle with "Core" issues, knowing exactly where their tax liability sits when selling across borders. We provide clarity for remote businesses, ensuring that digital sales are reported correctly and that international tax treaties are applied to prevent double taxation.

Foreign branches operating in the UAE have unique reporting requirements, often involving "Head Office" cost allocations, and international compliance standards. We ensure that your local filings are consistent with your global tax strategy while meeting all Multi-State Tax Compliance and international transparency rules.

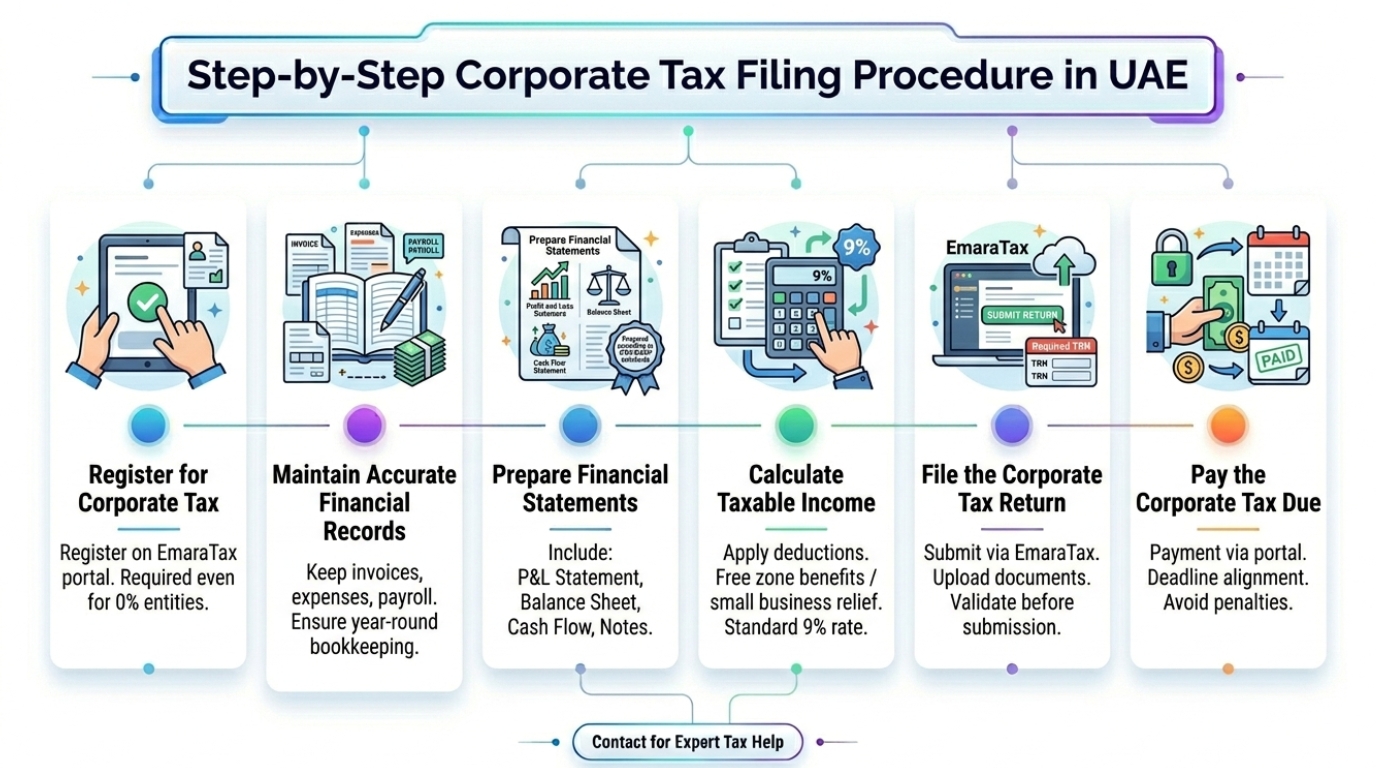

The UAE’s transition to a formal tax rule requires a disciplined approach to documentation and digital filing. To maintain compliance and protect your business license, every entity must follow a structured workflow within the Federal Tax Authority (FTA) ecosystem.

The first step for every business, including those operating within Free Zones, is to register via the EmaraTax portal. This registration is mandatory even for entities that qualify for a 0% Corporate Tax rate.

Failing to register by the FTA’s prescribed deadlines can result in an immediate AED 10,000 penalty, regardless of whether your business is currently profitable.

Compliance is built on year-round discipline, not a year-end scramble. Your business must maintain a digital trail of all sales invoices, deductible business expenses, and payroll records. Strong bookkeeping ensures that when it comes time to file, your data is audit-ready and aligns perfectly with your bank statements.

Accuracy at this stage prevents future inquiries. You must prepare a comprehensive set of financial documents, including:

| Financial Component | Core Function & Regulatory Purpose |

| Profit and Loss (P&L) Statement | To show your net taxable income and provide the basis for calculating the 9% corporate tax rate. |

| Balance Sheet | To reflect your company’s financial position, including all assets, liabilities, and equity at the end of the financial year. |

| Cash Flow Statement | To track the movement of liquidity and verify that the "on-paper" profit matches actual cash movement. |

| Notes to Financials | Providing essential context for specific line items, such as depreciation methods or related-party transactions. |

Standard Alignment: Mandatory for 2026: All statements must be prepared in accordance with IFRS or GAAP to meet the FTA’s transparency requirements.

Once your accounting is finalised, you must calculate your taxable profit by applying the relevant deductions and relief. While the standard 9% corporate tax rate applies to profits exceeding AED 375,000, many businesses may qualify for Small Business Relief or specific Free Zone benefits. Correctly identifying these incentives is the difference between overpaying and optimising your tax position.

The final submission is handled digitally through the EmaraTax portal. During this stage, you will use your Tax Registration Number (TRN) to access your profile, upload the required financial statements, and validate the data. Every figure must be double-checked; once submitted, any corrections may require a formal voluntary disclosure, which can attract further scrutiny.

If your taxable income exceeds the threshold, the final step is to settle the balance via the portal’s integrated payment gateways. Ensure that the payment is cleared, not just initiated, by the deadline to avoid late-payment interest charges, which currently accrue at an annualised rate of 14% in 2026.

Accuracy is meaningless if you are late. Under UAE law, your Corporate Tax return must be filed, and the tax must be paid within 9 months from the end of your relevant financial year. For businesses with a financial year ending December 31, the absolute deadline for submission is September 30 of the following year.

Choosing the right firm for your compliance needs is a decision that impacts your company's long-term financial health. At HFA Consulting, we don't just fill out forms; we build a protective barrier around your business. Our approach to business tax filing services is centred on precision, proactive strategy, and an obsession with detail that generic services simply cannot match.

Your filings are handled by FTA-registered tax agents and consultants who stay ahead of every regulatory update. We understand the specific nuances of the UAE Corporate Tax Law and the latest Cabinet Decisions, ensuring your business remains on the right side of the law. By utilising our deep expertise in Mainland and Free Zone structures, we ensure your entity is optimised for every available relief, including Small Business Relief and Qualifying Free Zone exemptions.

Accuracy is our baseline. Every return we prepare undergoes a multi-stage internal audit before it is submitted via the EmaraTax portal. This rigorous process has allowed us to achieve a 99% error reduction in financial records for our clients. We cross-verify your VAT data with your corporate tax entries to ensure there are no discrepancies that could trigger a manual review or a Tax Penalty.

Missing a deadline in 2026 is an expensive mistake, with late-payment interest now accruing at an annualised rate of 14%. Our proactive tracking system ensures you are notified months in advance of your Tax Deadline. We manage the entire timeline from closing your books to the final submission, so you never have to worry about the "9-Month Rule" or unexpected FTA enforcement actions.

Tax compliance shouldn't be a once-a-year conversation. We provide year-round advisory to help you understand how your daily business decisions impact your year-end liability. Whether it is managing Multi-State Tax Compliance or advising on Small Business Relief, our team is available to provide the insights you need to keep your business lean, profitable, and 100% compliant.

Even with the best intentions, administrative errors can spiral into significant hurdles. The FTA now utilises advanced data-matching tools to cross-check VAT returns against Corporate Tax filings. If these figures do not align perfectly, it triggers an automatic red flag for an audit.

Timing is the most frequent and costly mistake in the UAE. For a financial year ending December 31, your return must be filed by September 30 of the following year. Missing this 9-month rule triggers an immediate monthly penalty of AED 500 for the first year, which increases to AED 1,000 per month thereafter. In 2026, these fines are strictly enforced alongside an annualized 14% interest rate on any outstanding tax balance.

Many businesses fail to reconcile their audited financial statements with their tax returns, especially when separating "Qualifying" and "Non-Qualifying" income for Free Zones. If you exceed the de minimis threshold — the lower of 5% of revenue or AED 5 million — without precise reporting, you risk losing your 0% tax status entirely for five years.

Under the Tax Procedures Law, UAE businesses are required to maintain digital records for at least seven years. In 2026, the penalty for failing to provide these documents during a Federal Tax Authority (FTA) audit is AED 10,000 for the first offence. Records must be traceable and include a full audit trail for every transaction to prove the validity of your deductions.

A common error is failing to apply the 50% deduction limit on entertainment expenses or attempting to claim personal costs as business deductions. Furthermore, "Related Party" transactions must be strictly documented under Transfer Pricing rules. Failing to disclose these dealings, even if they are priced at "Arm's Length", invites intense regulatory scrutiny and potential adjustment penalties.

Many entities mistakenly believe that being "Loss-Making" or having "Exempt" status removes the need to file. This is incorrect; every registered business must file a return, even if it is a "Nil" return. Additionally, failing to register for a Tax Registration Number (TRN) within the FTA's prescribed timeline results in a flat AED 10,000 late-registration penalty.

Accountant

Client Accounting Manager

Clear answers to your most pressing questions about UAE Corporate Tax compliance, obligations, and strategic planning.

Compliance and clarity starts with accurate bookkeeping. If your records aren’t accurate, your business is headed for trouble. The good news? It only takes one decision to change the course.

Phone: 052 110 1467

Email: finance@hfaconsulting.ae

70+ Businesses served

Helped businesses gain compliance and smoother financial management.

20+ Active clients

Offering specialized financial consultancy services to businesses across UAE.

Let us know your challenge and business overview to get a proposal.