Zeeshan Khan

Zeeshan Khan Feb 23, 2026

Feb 23, 2026

Table of Contents

Managing a business in a VAT-active economy like the UAE means you aren’t just selling products; you’re essentially acting as a temporary guardian for the government’s tax revenue. At its core, Value Added Tax (VAT) is a consumption tax levied at every stage of the supply chain, from the raw material provider to the final retailer, ensuring that tax is collected in proportion to the value added at each step.

If you’ve ever felt confused by your tax returns, the secret lies in one simple equation: the difference between input and output VAT. While Output VAT is the tax you collect from customers on your sales, Input VAT is the tax you pay to your suppliers.

The magic happens in the middle: if you’ve paid more tax on your business expenses than you’ve collected from sales, you might be eligible for a VAT refund. Understanding this flow is the key to maintaining healthy cash flow and staying compliant with the Federal Tax Authority (FTA).

Understanding Input VAT: The Asset in Your Expenses

Input VAT is often the unsung hero of a business’s cash flow. While most people view taxes as a drain on resources, Input VAT actually represents a potential recovery of funds.

If you’re registered for VAT, every time you spend money on your business, you’re likely building up a “tax credit” that can be used to offset what you owe the government.

What exactly is Input VAT?

Input VAT is the Value Added Tax added to the price when you purchase goods or services for your business.

It is called “Input” because it relates to the items coming into your company, such as raw materials, office equipment, electricity, or even professional legal advice.

Essentially, you are paying this tax to your suppliers. However, unlike a standard consumer who pays VAT as a final cost, a VAT-registered business can usually treat this as a deductible expense against its tax liabilities.

When Does Input VAT Arise?

Input VAT isn’t triggered just by “spending money”; it arises specifically during transactions that involve taxable supplies. You will encounter Input VAT in the following scenarios:

- Local Purchases: Buying stationery, stock, or software from a vendor within your country.

- Imported Goods: When you bring products across the border, VAT is usually charged at the point of entry (though in places like the UAE, this is often handled via a “reverse charge mechanism”).

- Operating Expenses: Your monthly utility bills (water, electricity, and internet) and commercial rent typically carry Input VAT.

- Capital Assets: Buying a new delivery van or expensive machinery for your warehouse.

- Commercial Property: When purchasing or renting business premises, VAT on commercial property may apply, and it’s important to track this carefully to claim Input VAT correctly.

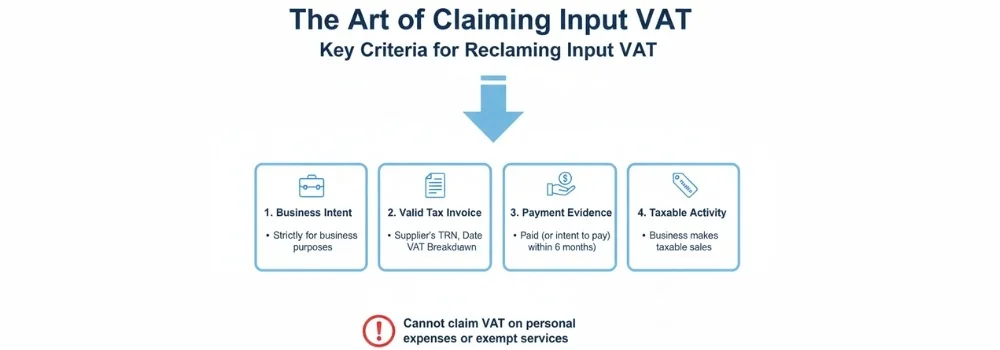

The Art of Claiming Input VAT

You don’t get the money back automatically; you have to “claim” it. To successfully reclaim Input VAT from the tax authorities, you must meet strict criteria:

- Business Intent: The purchase must be used strictly for business purposes. You cannot claim the VAT on your personal grocery bill just because you own a company.

- Valid Tax Invoice: This is the golden rule. You must possess a legal tax invoice that shows the supplier’s Tax Registration Number (TRN), the date, and a clear breakdown of the VAT amount.

- Payment Evidence: You must have actually paid (or be intended to pay) for the goods within a specific timeframe (usually 6 months in most jurisdictions).

- Taxable Activity: You can only claim Input VAT if your business makes taxable sales. If your business only provides “exempt” services (like certain financial or residential real estate services), you might not be able to claim Input VAT.

Real-World Example: The Calculation

Let’s look at how this works for a boutique coffee shop in Dubai.

Imagine the shop buys specialty coffee beans from a local wholesaler.

- Net Cost of Beans: 5,000 AED

- VAT (5%): 250 AED

- Total Paid to Supplier: 5,250 AED

In this scenario, the 250 AED is your Input VAT.

Later, when it’s time to file the tax return, the shop will use this 250 AED to reduce the total amount of tax they need to send to the FTA.

Output VAT: The Revenue Side of Taxation

If Input VAT is the tax you pay out, Output VAT is the tax you bring in. While it might feel like extra profit when you see it on your sales reports, it’s important to remember that this money belongs to the tax authorities.

Think of your business as a temporary custodian; you collect it from your customers at the point of sale and hold it until your next UAE VAT return filing, which is when you report and remit the collected Output VAT to the FTA. Timely and accurate filing ensures compliance and helps avoid penalties.

Managing Output VAT with precision is the hallmark of a professional, compliant business. It’s not just about adding a percentage to your price tag; it’s about understanding your legal obligation to the state.

What is Output VAT?

Output VAT is the Value Added Tax you charge on the sale of your goods or services. It is “output” because it relates to the products or services leaving your business and heading to the consumer.

Whether you are a wholesaler selling bulk electronics or a consultant providing marketing strategies, if your business is VAT-registered, you are legally required to add this tax to your invoices.

In the UAE, the standard rate for Output VAT is 5%. This tax is calculated on the sales price of the item before any tax is added (the “net” price).

When Does Output VAT Arise?

Output VAT isn’t a one-size-fits-all charge; it is triggered by specific business activities known as “taxable supplies.” You will typically see Output VAT arise in these moments:

- Standard Sales: Every time you sell a taxable product (like clothes, electronics, or food) to a customer.

- Service Fees: When you charge for professional services, such as accounting, legal advice, or maintenance work.

- Asset Disposals: If your business sells off old equipment, furniture, or a company vehicle, you must usually charge Output VAT on that sale.

- Deemed Supplies: In some cases, if you take business inventory for personal use or give away high-value gifts, the tax law may “deem” this a sale, requiring you to account for Output VAT.

Calculating Output VAT: The Formula

Calculating Output VAT is straightforward, but accuracy is non-negotiable. To find the amount you need to collect, you apply the tax rate to the total value of the goods or services provided.

The basic formula for a standard 5% VAT rate is:

Output VAT = Net Sales Amount (AED) X 0.05

If you have already quoted a “VAT inclusive” price to a customer and need to work backward to find the tax portion, the math changes slightly:

VAT Amount = Total Price (AED) − (Total Price (AED) ÷ 1.05)

Real-World Example: Output VAT in Action

Let’s look at a digital marketing agency based in Abu Dhabi. The agency signs a contract with a new client for a social media campaign.

- Service Fee (Net): 10,000 AED

- VAT Rate: 5%

- Output VAT Calculation: 10,000 × 0.05 = 500 AED

- Total Invoice Amount: 10,500 AED

In this scenario, the agency receives 10,500 AED from the client. While the agency keeps the 10,000 AED as revenue, the 500 AED is the Output VAT.

When the agency prepares its tax return at the end of the quarter, that 500 AED will sit on the “Liability” side of the balance sheet.

If the agency had no business expenses (Input VAT) to claim, they would owe the full 500 AED to the Federal Tax Authority (FTA).

Difference Between Input and Output VAT

The relationship between these two figures determines your final tax position. Here is a high-level comparison to help you categorize your transactions in AED:

| Basis | Input VAT | Output VAT |

| Meaning | Tax paid on purchases | Tax charged on sales |

| Who Pays | Business to supplier | Customer to business |

| Accounting Treatment | Asset (claimable) | Liability (payable) |

| Effect on VAT Payable | Reduces VAT payable | Increases VAT payable |

The Balancing Act:

- If Output VAT > Input VAT: You pay the difference to the FTA.

- If Input VAT > Output VAT: You are in a VAT refund position.

VAT Payable vs. VAT Refundable

When you reach the end of your tax period in the UAE, the journey of tracking input and output VAT converges into one final result: your net tax position. This is the moment you determine whether you owe the government a payment or if you are entitled to a VAT refund.

In the UAE, the Federal Tax Authority (FTA) requires businesses to settle this balance by submitting a VAT return, usually on a quarterly basis. Understanding which side of the fence you land on is essential for managing your business’s cash flow and ensuring you don’t leave money on the table.

Understanding the Outcomes

Two main scenarios occur when you balance your books:

1. VAT Payable (The Liability)

If your Output VAT (the tax you collected from sales) is higher than your Input VAT (the tax you paid on expenses), you have a surplus of tax money that belongs to the government.

- The Result: You must pay this difference to the FTA.

- Output VAT (AED) − Input VAT (AED) = VAT Payable

2. VAT Refundable (The Recovery)

If your Input VAT is higher than your Output VAT, it means you have paid more tax to your suppliers than you collected from your customers. This often happens to startups with high initial setup costs or companies that export goods (which are zero-rated).

- The Result: You are eligible for a VAT refund.

- Input VAT (AED) − Output VAT (AED) = VAT Refundable

Practical Illustration: A Step-by-Step Guide

To make this crystal clear, let’s follow a month in the life of a furniture manufacturer in Sharjah. This practical illustration shows exactly how the numbers move from a purchase to a sale, ending in a final computation.

Step 1: The Purchase Transaction (Input VAT)

The manufacturer buys premium timber from a local supplier to build dining tables.

- Cost of Timber (Net): 20,000 AED

- VAT at 5%: 1,000 AED

- Total Paid: 21,000 AED

- Result: The business now has 1,000 AED in Input VAT to claim.

Step 2: The Sale Transaction (Output VAT)

The manufacturer builds and sells five luxury dining tables to a local showroom.

- Sale Price (Net): 30,000 AED

- VAT at 5%: 1,500 AED

- Total Received: 31,500 AED

- Result: The business has collected 1,500 AED in Output VAT, which must be reported.

Step 3: The Net VAT Computation

At the end of the tax period, the accountant calculates the final position by subtracting the tax paid from the tax collected.

| Item | Amount (AED) |

| Total Output VAT (from Sales) | 1,500 |

| Total Input VAT (from Purchases) | -1,000 |

| Net VAT Position | 500 (Payable) |

Why Proper VAT Management Matters

Managing input and output VAT isn’t just about moving numbers from one column to another. In a modern economy, especially within the UAE’s rigorous regulatory framework, your VAT records are essentially a health report for your business. Neglecting this area doesn’t just lead to messy books; it can lead to severe legal and financial consequences.

Here is why professional VAT management is the backbone of a sustainable business.

1. Compliance with Tax Laws

The primary reason for meticulous VAT management is simple: it’s the law. When you register for VAT, you enter into a legal agreement with the state.

This requires you to charge the correct rate (5% in the UAE), understand the different types of VAT in UAE, issue valid tax invoices, and file your returns within strict deadlines. Proper management ensures that your “Input” claims are legitimate and your “Output” collections are fully reported, keeping you on the right side of the law.

2. Avoiding Penalties and Audits

Tax authorities, such as the Federal Tax Authority (FTA) in the UAE, HM Revenue & Customs (HMRC) in the UK, or the Bureau of Internal Revenue (BIR) in the Philippines, use sophisticated data-matching technology to spot inconsistencies.

If your input and output VAT figures don’t align with your bank statements or supplier reports, you trigger a “red flag that could result in a tax penalty. This is especially critical for VAT returns for startups in the UAE, where accurate reporting from the outset helps avoid fines and builds a strong compliance record.

- Fines: Late filings or incorrect data can result in penalties starting from thousands of dirhams.

- Audits: An unexpected tax audit can halt business operations for weeks as officials scrutinize every receipt. Proper management keeps your “audit trail” clean and ready.

3. Maintaining Accurate Financial Records

VAT management forces a level of discipline that benefits your entire company. When you track every filing of Input VAT, you are essentially tracking every business expense.

- Cash Flow Visibility: Knowing your VAT payable or refundable position helps you set aside the right amount of cash for the end of the quarter.

- Profitability Analysis: It allows you to see your true margins. If you aren’t accounting for the VAT you pay on overheads, your “net profit” might be lower than you realize.

4. The Role of Tax Authorities

Tax authorities are not just collectors; they are regulators of the economy. Entities like the FTA or HMRC provide the framework that ensures a level playing field. By enforcing VAT rules, they ensure that your competitors aren’t gaining an unfair advantage by skipping taxes.

Understanding their role helps you view VAT as a standard cost of doing business in a global market rather than an arbitrary hurdle.

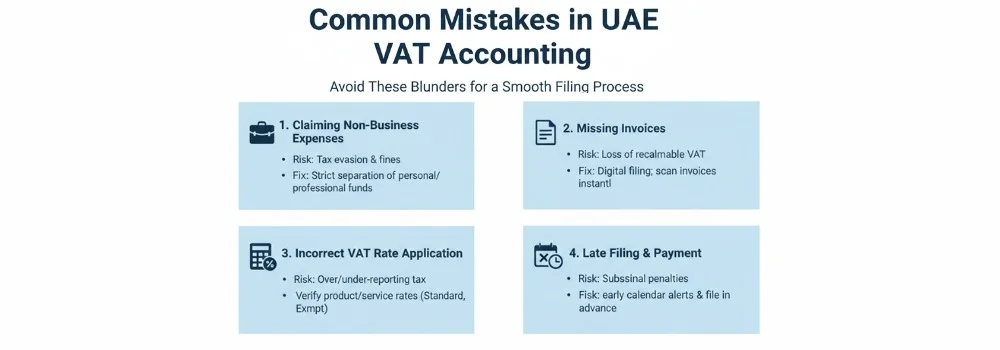

Common Mistakes in VAT Accounting

Even the most seasoned entrepreneurs can trip up on the complexities of tax law. When it comes to input and output VAT, a single misplaced digit or a forgotten receipt can lead to a domino effect of financial errors.

In the UAE, where the FTA (Federal Tax Authority) maintains a high standard for documentation, avoiding these common blunders is essential for smooth filing and accurate VAT accounting in the UAE. Proper bookkeeping, organized invoices, and careful reconciliation are key to ensuring your VAT records are complete and compliant.

1. Claiming Non-Business Expenses

One of the most frequent errors is attempting to claim Input VAT on personal purchases. Whether it’s a family dinner or a personal laptop, if the expense isn’t used for “conducting business,” it isn’t claimable.

- The Risk: The FTA views this as tax evasion.

- The Fix: Maintain a strict “wall” between personal and professional finances. If an item is for mixed use (like a mobile phone), only claim the portion used for business.

2. Missing Invoices

You might have paid the VAT, but if you don’t have the paperwork, it didn’t happen. To claim Input VAT, you must possess a valid Tax Invoice that includes the supplier’s TRN, the date, and the specific VAT amount in AED.

- The Risk: Losing out on thousands of dirhams in potential credits because you lost a receipt or accepted a “pro-forma” invoice instead of a final tax invoice.

- The Fix: Implement a digital filing system where invoices are scanned and uploaded the moment they are received.

3. Incorrect VAT Rate Application

While 5% is the standard rate for input and output VAT in the UAE, it isn’t the only rate. Applying 5% to a “zero-rated” export or an “exempt” financial service is a common mistake that throws off your entire return.

- The Risk: Overcharging customers (making you less competitive) or under-reporting tax (leading to fines).

- The Fix: Regularly review the nature of your products. Are they standard-rated, zero-rated (like international exports), or exempt (like certain residential land)?

4. Late Filing and Payment

Procrastination is the most expensive mistake in VAT accounting. Missing a filing deadline or failing to transfer the VAT payable balance on time triggers immediate penalties.

- The Risk: In the UAE, late filing penalties can be substantial, and they often increase the longer the payment remains outstanding.

- The Fix: Set calendar alerts at least 10 days before your tax period ends. Aim to file early to allow for any technical glitches on the government portal.

Choosing the Right VAT Consultant for Your Business

Selecting a partner to manage your tax affairs is one of the most critical decisions you will make for your company’s long-term stability. While the digital landscape in the UAE makes it easier to track transactions, the nuance of evolving laws requires a specialized touch to avoid costly errors.

When looking for VAT consultancy services in Dubai, you need a team that doesn’t just process paperwork but understands the strategic flow of your specific industry.

This is where HFA Consulting excels, providing a proactive approach that bridges the gap between complex FTA regulations and your daily operations.

By choosing a consultant with deep local expertise, you ensure that your input and output tax reconciliations are always audit-ready, allowing you to focus on scaling your business with complete peace of mind.

Conclusion

Understanding the internal mechanics of input and output VAT is not just a matter of compliance; it is a fundamental pillar of business intelligence. By clearly distinguishing between the tax you pay on expenses (Input) and the tax you collect on sales (Output), you gain the ability to manage your cash flow effectively and identify opportunities for a VAT refund.

The final takeaway for every entrepreneur is that while businesses act as the essential collectors and conduits for these funds, Value Added Tax is a consumption tax ultimately borne by the final consumer.

Handling this cycle with precision, from accurate record-keeping to timely filing, ensures your business remains a healthy, transparent, and profitable part of the economic supply chain.

FAQs

What is Value Added Tax (VAT)?

Value Added Tax (VAT) is a consumption tax charged on goods and services at each stage of production and distribution. In the UAE, VAT is charged at a standard rate of 5% on most goods and services.

What is the difference between Input VAT and Output VAT?

Input VAT is the tax a business pays to suppliers when purchasing goods or services. Output VAT is the tax a business collects from customers when selling goods or services. The difference between these two determines how much VAT a business needs to pay or claim back.

How is Input VAT calculated?

Input VAT is calculated by applying the 5% VAT rate to the cost of business purchases. For example, if you purchase goods worth 2,000 AED, the Input VAT would be 100 AED.

How is Output VAT calculated?

Output VAT is calculated by applying the 5% VAT rate to the selling price of goods or services. For example, if you sell goods worth 5,000 AED, the Output VAT collected would be 250 AED.

How do you compute VAT payable?

The formula is: Total Output VAT – Total Input VAT = VAT Payable. If input VAT exceeds output VAT, the difference is a refundable credit.

If Output VAT is higher than Input VAT, the difference must be paid to the Federal Tax Authority (FTA). If Input VAT is higher than Output VAT, the business may be eligible for a VAT refund.

Zeeshan Khan

My name is Zeeshan Khan, and I’m a UAE-based business and tax consulting professional with hands-on experience in VAT compliance, corporate tax advisory, business setup, and regulatory services. I work closely with startups, SMEs, and established companies to help them navigate UAE tax laws, improve compliance, and make informed financial decisions. With a strong understanding of FTA regulations, corporate structuring, and commercial taxation in the UAE, my focus is on translating complex laws into clear, practical guidance for business owners. Through my writing, I aim to provide accurate, up-to-date insights that help businesses stay compliant, reduce risk, and operate confidently in the UAE market.