Zeeshan Khan

Zeeshan Khan Mar 20, 2026

Mar 20, 2026

Table of Contents

Keeping up with the UAE’s shifting business landscape can feel like a full-time job. Not long ago, the Emirates was known as a purely tax-free haven, but things are changing fast. If you’re a business owner, a freelancer, or an investor, you’ve likely heard whispers about the UAE’s new tax rules.

These updates aren’t just about collecting revenue; they are a strategic move to align the country with global transparency standards and diversify the economy. But what do these rules and regulations of the new tax in uae actually mean for your bank account and your operations?

The shift can be confusing. Are you wondering if your current setup still complies with UAE tax rules? Whether it’s navigating the UAE tax residency rules to determine where you owe money or understanding the specific UAE federal tax authority rules that govern your filing, the “wait and see” approach is no longer an option.

From small startups to massive corporations, everyone is now asking: “How do I adapt to the new tax rule in the UAE without getting hit by penalties?” The solution lies in staying ahead of the curve and mastering the tax rules in the UAE before they catch you.

Overview

A 9% federal corporate tax now applies to business profits over AED 375,000, starting from financial years on or after June 1, 2023. To meet global standards, a 15% minimum top-up tax for large multinationals begins in 2025.

Additionally, 2026 updates bring a five-year statute of limitations on tax claims, revised penalties, and updated VAT compliance rules.

Key UAE Tax Rule Changes in 2026

Staying compliant is the only way to avoid heavy fines under the UAE Federal Tax Authority rules. Here is a breakdown of the specific shifts you need to know:

New VAT Law Amendments

Under Federal Decree-Law No. 16 of 2025, the focus has shifted heavily toward transparency. These tax rules in the UAE now prioritize strict anti-evasion measures. If your business isn’t keeping crystal-clear records, you could be flagged during a routine check.

Five-Year Deadline for VAT Refunds

Timing is everything when it comes to your bottom line. One of the most critical UAE tax rules is the new five-year “use it or lose it” policy. This means you must claim your VAT refunds within a strict five-year window.

If you miss this deadline, the risk is absolute: those expired credits are gone forever and can no longer be used to offset your future payments.

Changes to the Reverse Charge Mechanism

To make life easier for certain sectors, the government has simplified invoicing requirements for specific transactions. This new tax rule in the UAE reduces the paperwork burden on businesses, provided they follow the updated electronic filing standards.

Stronger Audit and Compliance Powers

The authorities now have expanded rights to look into your books. There is a much sharper focus on fraud prevention, meaning your documentation must be ready for an audit at any time. Think of it as a move from “self-reporting” to “active verification.”

Input Tax Recovery Restrictions

Are you clear on the UAE VAT input tax credit rules? There is now a zero-tolerance policy for evasion. If a business is found to be involved in tax evasion, it completely loses the right to recover any input VAT. In short, if you don’t play by the rules, you pay the full price without any deductions.

UAE Corporate Tax Rules (Current Structure)

The introduction of federal corporate tax marks a significant shift in how companies operate within the Emirates. This framework is designed to ensure the UAE remains a leading global hub for business while meeting international tax transparency standards.

Instead of a blanket tax on all income, the system uses a tiered approach to support smaller businesses and startups while ensuring larger entities contribute their fair share.

Tax Rates

Understanding your tax liability depends entirely on your annual net profit. Currently, the rates are split into two main brackets:

0% on profits up to AED 375,000:

This threshold is specifically designed to reduce the burden on small businesses and entrepreneurs, allowing them to reinvest more of their earnings into growth.

9% on profits above AED 375,000

Any profit exceeding this amount is subject to the standard statutory rate. It is a competitive rate globally, aimed at maintaining the UAE’s attractiveness to foreign investors.

Compliance and Reporting Requirements

Under the UAE federal tax authority rules, compliance is no longer optional. Every taxable person, including those in Free Zones, must register for Corporate Tax and obtain a Tax Registration Number.

You are required to file a tax return for each financial period, usually within nine months of the end of that period. Keeping accurate financial records is essential, as these documents form the basis of your filings and are necessary if you are ever selected for a small business audit.

Upcoming E-Invoicing System in the UAE

The way you handle paper and PDF invoices is about to change forever. The UAE is launching a nationwide digital invoicing initiative to modernize how financial data is shared between businesses and the government.

This isn’t just a minor update; it’s a move toward a “paperless” tax environment where every transaction is recorded in real-time.

Digital Invoicing Initiative

This system moves beyond simple digital files. Under the new UAE federal tax authority rules, an e-invoice is a structured data file (like XML) that is instantly validated and exchanged between the supplier, the buyer, and the FTA.

This “5-corner model” ensures that every transaction is recorded accurately and securely, leaving no room for manual errors or hidden records.

Implementation Timeline Starting 2026

Preparation is key, as the rollout happens in specific stages. A pilot program for selected businesses and voluntary adopters begins on July 1, 2026, giving early movers a chance to test their systems in a live environment before the mandates kick in.

Mandatory Phase January 2027

The first mandatory wave begins on January 1, 2027, for large businesses with an annual revenue of AED 50 million or more. These companies must have an Accredited Service Provider (ASP) appointed by July 31, 2026, to ensure they are ready for the switch.

Full Rollout July 2027

By July 1, 2027, the rules will extend to all other taxpayers with revenue below the AED 50 million threshold. Government entities will follow shortly after in October 2027. If you fall into this group, you must appoint your ASP by March 31, 2027, to avoid significant monthly penalties for non-compliance.

Benefits for Transparency and Reporting

The move to e-invoicing is designed to slash manual errors and make tax reporting almost instantaneous. For your business, this means faster payment cycles and a massive reduction in processing costs, with some estimates suggesting up to 66% in savings.

For the authorities, it provides a clear, tamper-proof audit trail, making it much harder for fraud or tax evasion to slip through the cracks. It essentially creates a fairer, more efficient market where compliance is built directly into your daily workflow.

Excise Tax Updates

The UAE has officially shifted its strategy for taxing sweetened beverages. Moving away from a flat-rate model, the government has introduced a tiered volumetric tax system effective from January 1, 2026.

This change is specifically designed to target the sugar content in drinks, rewarding manufacturers who offer healthier options while increasing the cost for high-sugar products.

New Tiered Tax System for Sugary Drinks

Instead of a simple percentage-based tax, beverages are now categorized into tiers based on the amount of sugar they contain per 100ml. This system applies to all ready-to-drink beverages, as well as powders, gels, and concentrates.

High Sugar Category

Drinks containing 8g or more of sugar per 100ml fall into this tier. These products face the highest excise rate of AED 1.09 per liter. This category typically includes regular sodas and high-sugar energy drinks.

Moderate Sugar Category

Beverages with a sugar content between 5g and less than 8g per 100ml are taxed at a reduced rate of AED 0.79 per liter. This tier is intended to nudge manufacturers toward modest reformulations that reduce sugar levels without changing the product’s core identity.

Low and Zero Sugar Category

If a drink contains less than 5g of sugar per 100ml, it qualifies for the 0% excise rate. Similarly, beverages that use only artificial sweeteners (with no added sugar) are also exempt from this tax. This makes low-calorie and diet options much more price-competitive on the shelf.

Impact on Beverage Manufacturers and Retailers

For manufacturers, this change is a major incentive for product reformulation. Reducing sugar by just a few grams per serving can move a product into a lower tax bracket, significantly lowering the “landed cost” and allowing for better retail pricing.

Retailers and importers face a new administrative hurdle: the mandatory Emirates Conformity Certificate. Every beverage must now have a lab report from an accredited facility verifying its sugar content.

Without this certificate, the Federal Tax Authority (FTA) will automatically classify the drink as “High Sugar” and apply the maximum tax rate of AED 1.09 per liter by default. This makes accurate documentation and inventory management more critical than ever to protect profit margins.

How UAE Tax Rule Changes Affect Businesses

Adapting to the UAE’s new tax rules is no longer just a task for your accounting department; it’s a core business strategy.

Every decision you make, from pricing to contract terms, is now filtered through the lens of these updated rules and regulations of the new tax in uae. Here is how these shifts practically change your daily operations.

Compliance Requirements

The burden of proof has shifted. Under the UAE federal tax authority rules, businesses are expected to maintain digital-ready records that can be audited at a moment’s notice.

This means moving away from manual spreadsheets and adopting FTA-compliant accounting software. You must ensure your registration for both VAT and Corporate Tax is current and that your UAE tax residency rules status is clearly defined to avoid double taxation or residency disputes.

Financial Planning and Accounting Updates

Your profit margins may look different under the tax rules in uae. With the 9% corporate tax on profits over AED 375,000, businesses must now factor in tax liabilities during their annual budgeting.

Furthermore, understanding the UAE VAT input tax credit rules is vital for cash flow management. If you don’t correctly account for the VAT you pay on business expenses, you are essentially leaving money on the table or worse, creating a deficit in your filings.

Risk of Penalties for Non-Compliance

The cost of a mistake has never been higher. The new tax rule in the UAE includes a revised administrative penalty framework designed to discourage late filings and incorrect data submission. Understanding the UAE Corporate Tax penalty provisions is essential for businesses to avoid unnecessary fines. Beyond just penalties, there is also a reputational risk; the FTA has increased its audit powers to identify fraud and evasion.

If a business is caught intentionally breaking the UAE tax rules, the penalties can include massive surcharges and the permanent loss of the right to recover input tax. Staying compliant isn’t just about following the law; it’s about protecting your business’s future.

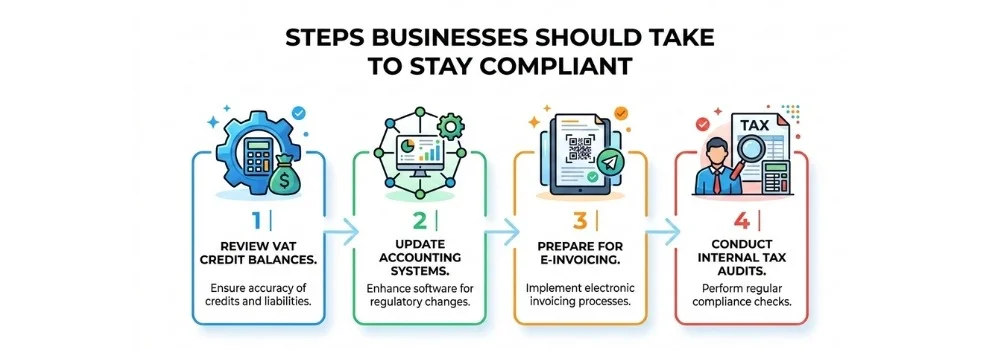

Steps Businesses Should Take to Stay Compliant

Staying ahead of the UAE’s new tax rules requires a proactive approach rather than a reactive one. To protect your business from penalties and ensure smooth operations, you should focus on these four critical areas immediately.

Review VAT Credit Balances

Under the updated UAE VAT input tax credit rules, you have a strict five-year window to claim your refunds. It is essential to conduct a thorough review of your historical VAT records to identify any unclaimed input tax.

If you have credits approaching that five-year limit, you must act now; otherwise, those funds will be permanently forfeited and cannot be used to offset future tax liabilities.

Update Accounting Systems

Your old spreadsheets may no longer cut it. To comply with UAE Federal Tax Authority rules, your accounting software must be capable of generating the structured data required for modern reporting and aligned with accounting standards in UAE.

This includes the ability to track profit thresholds for corporate tax and handle the complexities of the new tax rule in uae. Updating your systems now ensures that your financial reporting is accurate, automated, and ready for the next filing season.

Prepare for E-Invoicing

With the digital invoicing initiative rolling out in stages starting in 2026, the time to prepare is today. You should begin evaluating Accredited Service Providers (ASPs) who can integrate with your current systems.

Transitioning early allows your team to get comfortable with the “5-corner model” of real-time validation before it becomes a legal requirement. Being an early adopter can also improve your relationship with vendors who prefer faster, digital payment cycles.

Conduct Internal Tax Audits

Don’t wait for the authorities to knock on your door. Conducting a regular internal audit is the best way to identify gaps in your compliance before they become costly problems.

Review your UAE tax residency rules status, verify your import tax rules UAE documentation, and ensure every transaction has the correct supporting evidence. An internal check-up helps you catch manual errors, prevent fraud, and ensure your business is “audit-ready” at all times.

Common Mistakes Businesses Should Avoid

Even well-intentioned businesses can fall into traps that lead to unnecessary costs. Avoiding these common pitfalls is the easiest way to stay on the right side of the UAE Federal Tax Authority rules.

Missing Refund Deadlines

One of the most expensive errors a company can make is failing to track the calendar. As per the UAE tax rules, you have exactly five years to claim your VAT refunds.

Many businesses treat these credits as a permanent asset on their balance sheet, but the new “use it or lose it” policy means they can vanish. If your internal tracking isn’t flagging old credits, you are effectively giving away your hard-earned cash back to the state.

Incorrect VAT Filings

Errors in reporting are a major red flag for authorities. This often happens when businesses don’t fully understand the UAE VAT input tax credit rules or miscalculate the tax on imported goods, especially when they file VAT in UAE without proper reconciliation.

Filing an incorrect return, even by mistake, can trigger audits and lead to administrative penalties. It’s not just about the numbers; it’s about applying the right tax rules in the UAE to the right transaction.

Poor Documentation

If it isn’t documented, as far as the tax man is concerned, it didn’t happen. Many businesses struggle during audits because they lack valid tax invoices, proof of payment, or proper contracts.

With the UAE’s new tax rules moving toward digital transparency, keeping “shoebox” receipts or unorganized folders is a recipe for disaster. Proper documentation is your only defense if the authorities question your UAE tax residency rules or your business expenses.

Who to Consult for Tax Consultancy in the UAE

Staying on top of the UAE new tax rules doesn’t have to be a solo struggle. Many businesses work with professional tax consultants in dubai to ensure every filing is accurate and timely.

Expert firms like HFA Consulting provide the technical support needed to manage the rule of tax agent in UAE , helping you handle everything from corporate tax registration to complex VAT audits.

By partnering with a specialized consultancy, you bridge the gap between reading the law and applying it correctly, ensuring you remain fully compliant with the uae federal tax authority rules while you focus on your business goals.

Conclusion

The UAE new tax rules represent a major leap toward a more transparent and globally aligned economy. From the 9% corporate tax threshold to the strict five-year window for VAT refunds and the upcoming e-invoicing mandate, the requirements for doing business in the Emirates have changed.

Staying compliant with these new tax rule in uae updates is no longer just about avoiding penalties; it is about ensuring your business remains credible and operationally sound in a digital-first regulatory environment.

By acting now auditing your records, updating your systems, and understanding the UAE federal tax authority rules you can turn these regulatory changes into a foundation for long-term stability and growth.

FAQs

What are the new tax rules in the UAE for 2026?

The 2026 updates introduce a strict five-year deadline for VAT refunds, a new tiered excise tax on sugary drinks, and expanded audit powers for the authorities. They also focus on a digital-first approach to reporting and stricter anti-evasion measures.

Has the UAE increased VAT?

No, the standard VAT rate remains at 5%. However, the uae tax rules have been updated to change how certain credits are claimed and how specific industries, like the beverage sector, are taxed through excise duties.

Who must pay corporate tax in the UAE?

Most businesses and individuals with a commercial license must pay. Currently, a 0% rate applies to profits up to AED 375,000, while a 9% rate applies to any profits exceeding that amount. Free Zone entities may also be subject to these rules depending on their “Qualifying Income.”

When will e-invoicing become mandatory?

It begins with a pilot phase in July 2026. Mandatory implementation for large businesses (revenue over AED 50 million) starts in January 2027, with all other taxpayers expected to comply by July 2027.

Zeeshan Khan

My name is Zeeshan Khan, and I’m a UAE-based business and tax consulting professional with hands-on experience in VAT compliance, corporate tax advisory, business setup, and regulatory services. I work closely with startups, SMEs, and established companies to help them navigate UAE tax laws, improve compliance, and make informed financial decisions. With a strong understanding of FTA regulations, corporate structuring, and commercial taxation in the UAE, my focus is on translating complex laws into clear, practical guidance for business owners. Through my writing, I aim to provide accurate, up-to-date insights that help businesses stay compliant, reduce risk, and operate confidently in the UAE market.